Enterprise AI Adoption Statistics

Last updated on July 6, 2026

Enterprise AI adoption statistics for 2026 tell two different truths at the same time: AI is now normal inside large organizations, and mature deployment is still much rarer than executive enthusiasm suggests.

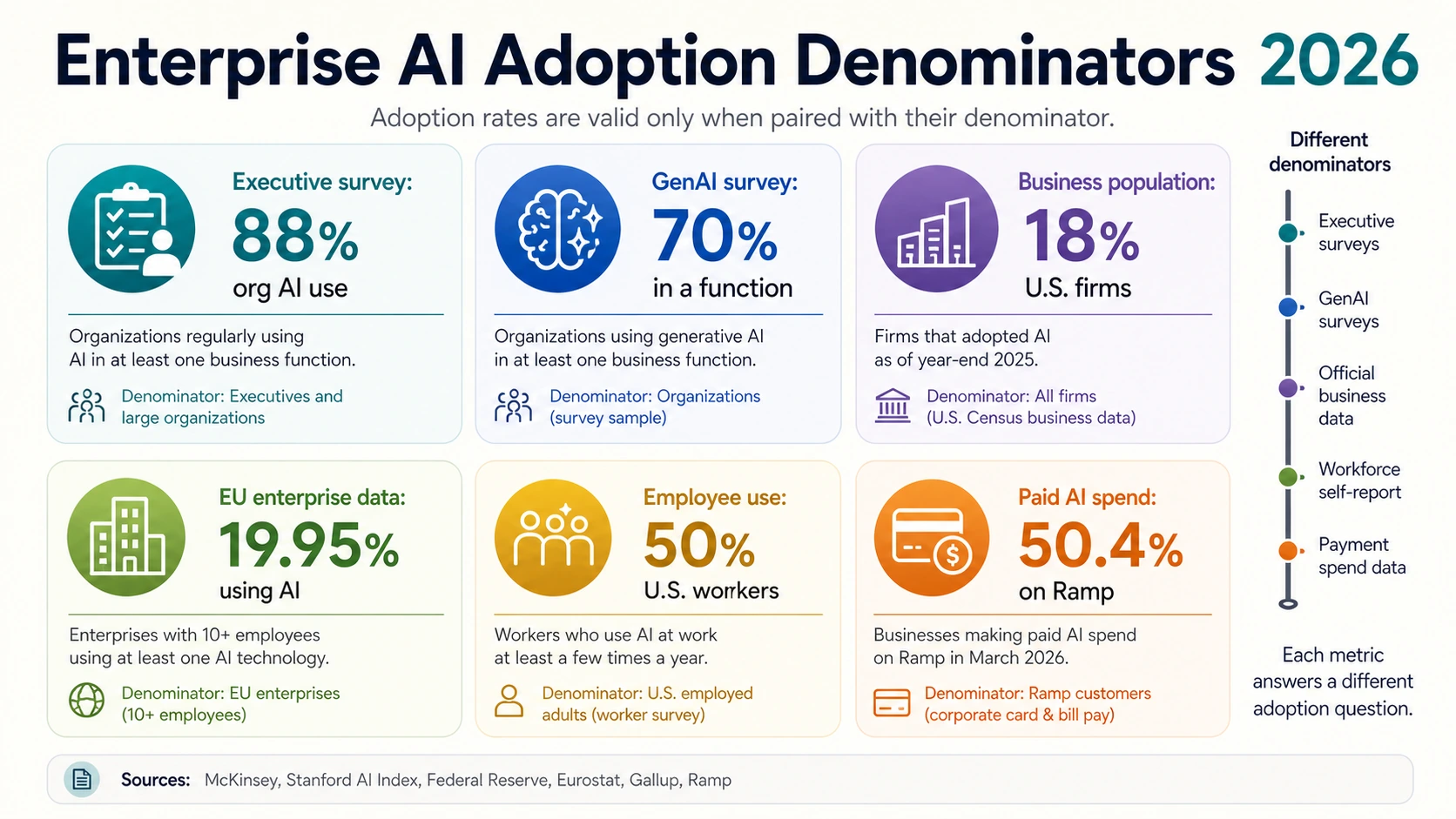

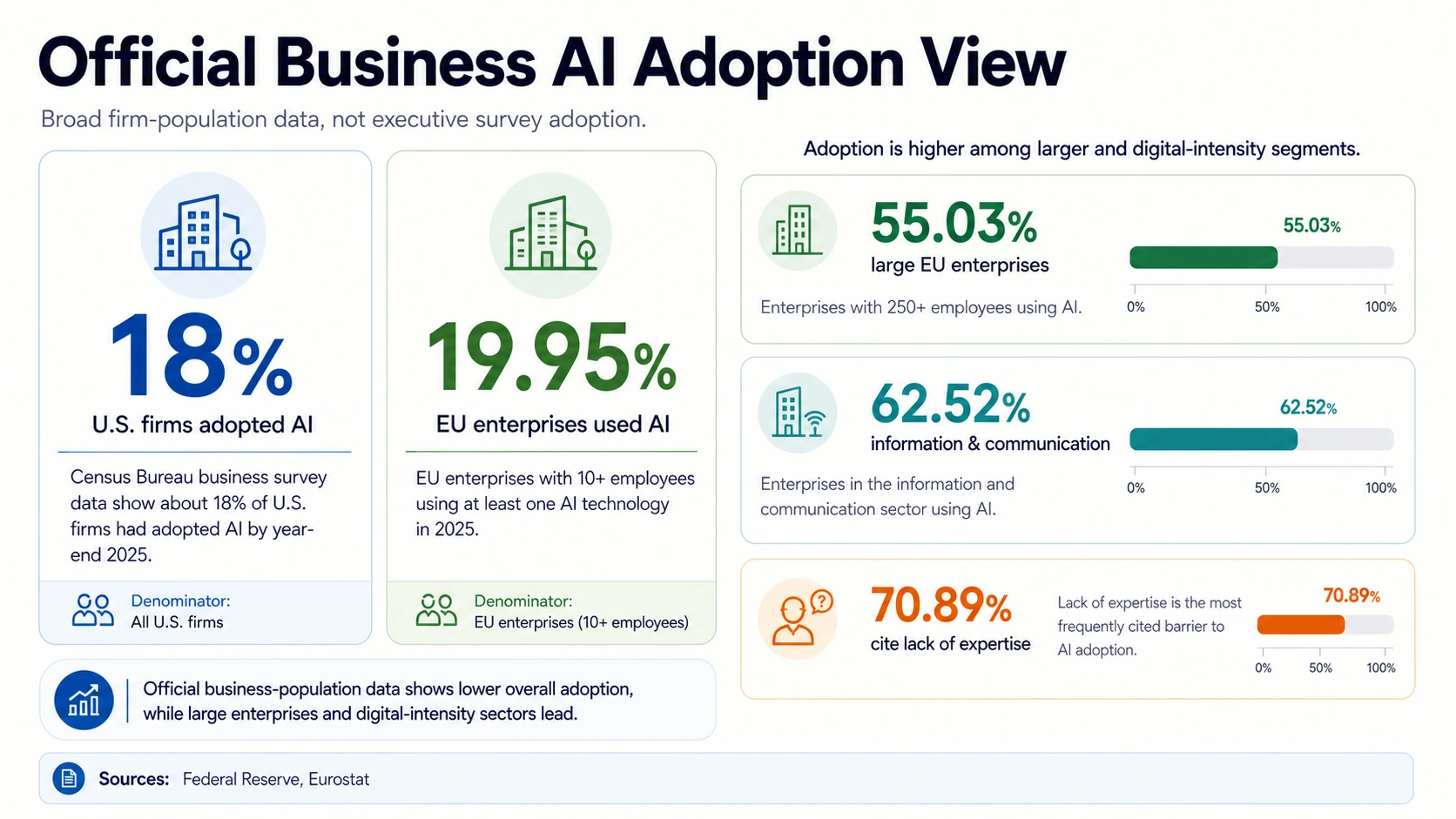

The broadest management surveys show AI use almost everywhere. McKinsey found that 88% of organizations regularly use AI in at least one business function, and the Stanford AI Index reports 88% organizational adoption and 70% generative AI use in at least one function. Official business surveys are far more conservative because they count every firm, not only larger or tech-forward respondents: a Federal Reserve review of Census data estimates that about 18% of U.S. firms had adopted AI by the end of 2025, and Eurostat reports that 19.95% of EU enterprises used AI in 2025.

That gap is the whole story. Enterprise leaders are no longer asking whether AI matters. They are deciding where it can survive procurement, data access, legal review, workflow redesign, cost control, and governance. The most useful enterprise AI adoption statistics separate six questions: who has tried AI, who has paid for AI, who has AI inside production workflows, who can measure ROI, who has governance that matches autonomy, and who has redesigned work around AI rather than bolting a chatbot onto old processes.

Enterprise AI Adoption In 2026: The Big Picture

The headline adoption numbers use different denominators, so read them as separate survey, official, employee, and spend signals rather than one figure.

Adoption, scaling & agents (2026 surveys)

ROI, spend & readiness (2026 surveys)

Enterprise AI Adoption Depends On The Denominator

The single most important habit when reading enterprise AI adoption statistics is to ask what population each number counts. The same phrase — “AI adoption” — can mean executive-survey exposure, broad firm-population use, individual employee behavior, or paid-tool spend, and those four denominators produce numbers that differ by more than four times.

The highest adoption numbers usually come from executive surveys and large-company samples. McKinsey’s 88% regular AI use is best read as the share of surveyed organizations with AI active somewhere, not the share of every firm in the economy running production-grade AI. Stanford’s 70% generative AI use in at least one function tells the same story: AI has entered the operating model of many organizations, but the denominator is weighted toward organizations mature enough to appear in global AI surveys.

Official statistical agencies use a different denominator. The Federal Reserve’s review of U.S. data points to about 18% of firms adopting AI by the end of 2025. Eurostat reports 19.95% of EU enterprises using AI in 2025. These numbers include many small firms with neither dedicated data teams nor AI procurement programs, and they rely on stricter survey definitions than a manager saying employees use ChatGPT.

Employee-level statistics add a third denominator. Gallup reports that half of employed Americans use AI at least a few times a year, while 28% use it a few times a week or more and 13% use it daily. Salesforce’s Slack Workforce Index says 60% of desk employees use AI, with daily use far above the prior year. These are not enterprise deployment rates. They show that employees are pulling AI into work before every organization has a formal platform strategy.

Spend data creates a fourth view. Ramp’s business payment data showed its AI Index crossing 50.4% in March 2026, meaning just over half of sampled businesses had measurable AI-related vendor spend — up from 43.3% in July 2025. That is much higher than Census business survey rates because payments capture software purchases rather than the full business population’s self-reported use. Menlo Ventures’ $37 billion enterprise generative AI spend estimate confirms budgets have moved, but budget movement is still not the same as workflow maturity.

Read every number by its own denominator

Enterprise AI adoption figures answer different questions. Tap a lens to see what it measures — and what it does not prove.

McKinsey, Eurostat, Federal Reserve, Gallup, RampThe practical reading is simple: 2026 is not a year of early curiosity for enterprise AI. It is a year of uneven institutionalization. Large-company survey adoption, employee usage, official business adoption, payment data, and production deployment all measure real behavior, but each one answers a different question.

Broad Adoption Is Real, But Scaling Is Narrower

McKinsey’s 2025 survey is one of the clearest signals that AI has become a mainstream enterprise tool. Beyond 88% regular AI use, more than two-thirds of AI-using organizations use AI in more than one function and about half use it in three or more. AI is no longer isolated in data science or innovation labs; it has moved into IT, marketing and sales, service operations, knowledge management, product development, and internal productivity.

Yet the same data shows the scaling gap. Only about one-third of surveyed organizations were scaling AI programs, and only 39% reported enterprise-level EBIT impact — usually less than 5%. The pattern is not failure. It is diffusion without full redesign.

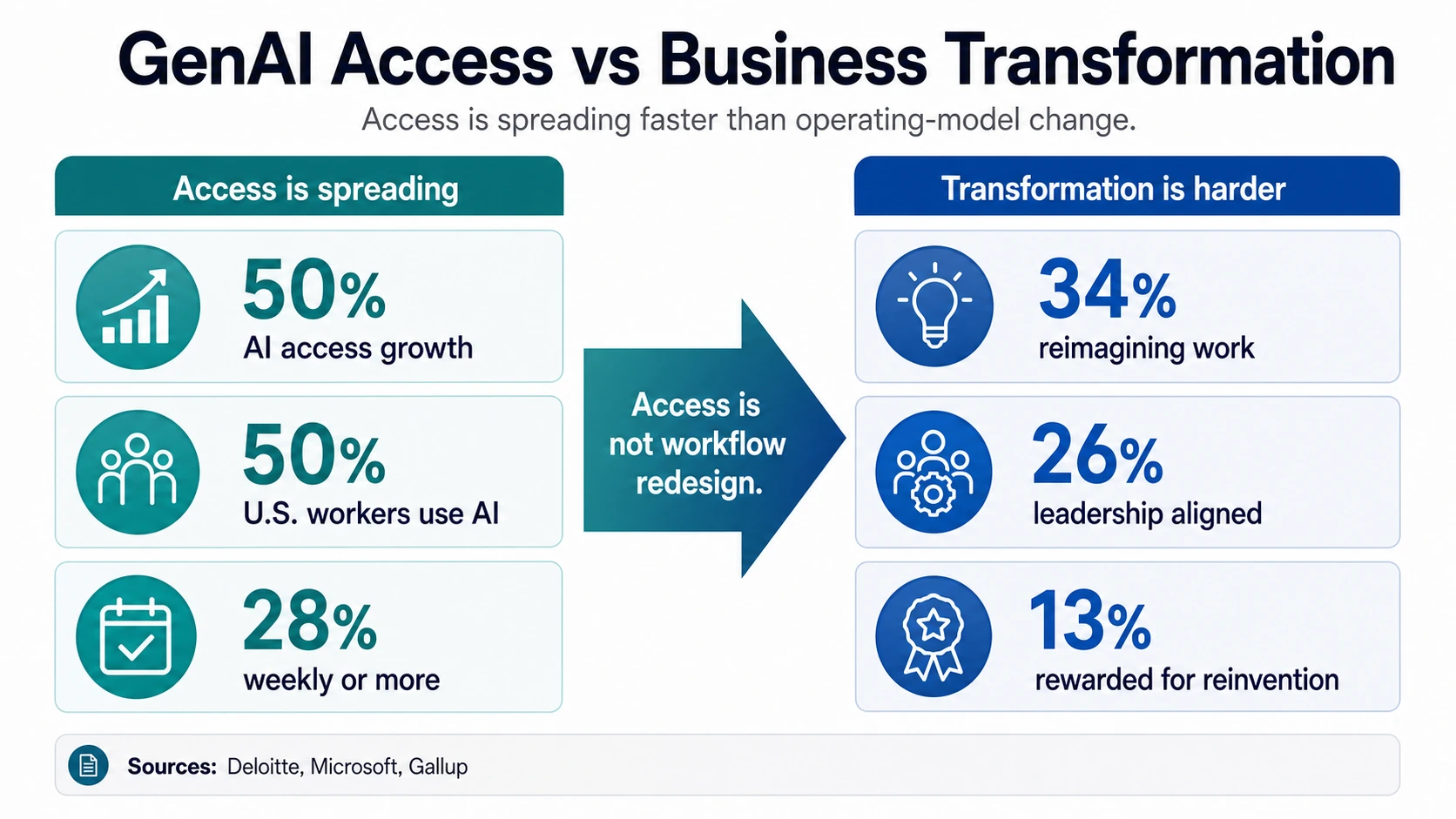

Deloitte reports a similar split. Employee AI access rose 50% in 2025, and the share of companies with at least 40% of AI projects in production was expected to double in six months. At the same time, Deloitte says only 34% of organizations are truly reimagining the business around AI. Access is spreading faster than operating-model change.

Microsoft’s Work Trend Index gives a workforce-level reason for that gap. Only 26% of AI users said leadership was aligned, while 65% feared falling behind and only 13% felt rewarded for reinvention. Employees may have tools, but organizations often lack the incentives, workflow documentation, and managerial permission needed to change the work itself.

Enterprise GenAI Access Is Outrunning Formal Change

Generative AI has spread unusually fast because employees can use it before a central program is ready. The Federal Reserve notes that real-time population survey data showed 41% work-related generative AI adoption in November, while business survey estimates suggested a smaller share of firms had formal AI adoption. That mismatch is one reason enterprise AI feels both everywhere and incomplete.

The MIT NANDA report describes a related pattern in large organizations. It says more than 80% of organizations explored or piloted ChatGPT or Copilot, nearly 40% deployed those tools, and roughly 40% purchased official LLM subscriptions. But employees from more than 90% of surveyed companies reported regular personal AI tool use, while only 5% of custom enterprise AI tools reached production. The numbers are directional, but they capture a real behavior: employees adopt usable tools faster than companies can integrate custom systems.

Asana’s Work Innovation Lab data also shows executive use running ahead of the broader workforce. It reports that 52% of executives use AI weekly, compared with 36% of knowledge employees overall, with 30% using AI for data analysis and 25% for administrative tasks. That points to a practical adoption pattern: AI starts with personal productivity, analysis, writing, summarization, and administrative acceleration before it becomes a fully governed workflow layer.

Salesforce’s Slack Workforce Index reports that 40% of desk employees have worked with an AI agent, and 23% have offloaded tasks to one. Those are meaningful signals, but they do not mean most enterprises have autonomous agent operations. They mean the interface between employees and AI is changing quickly — people increasingly assign, check, and combine AI outputs inside everyday work.

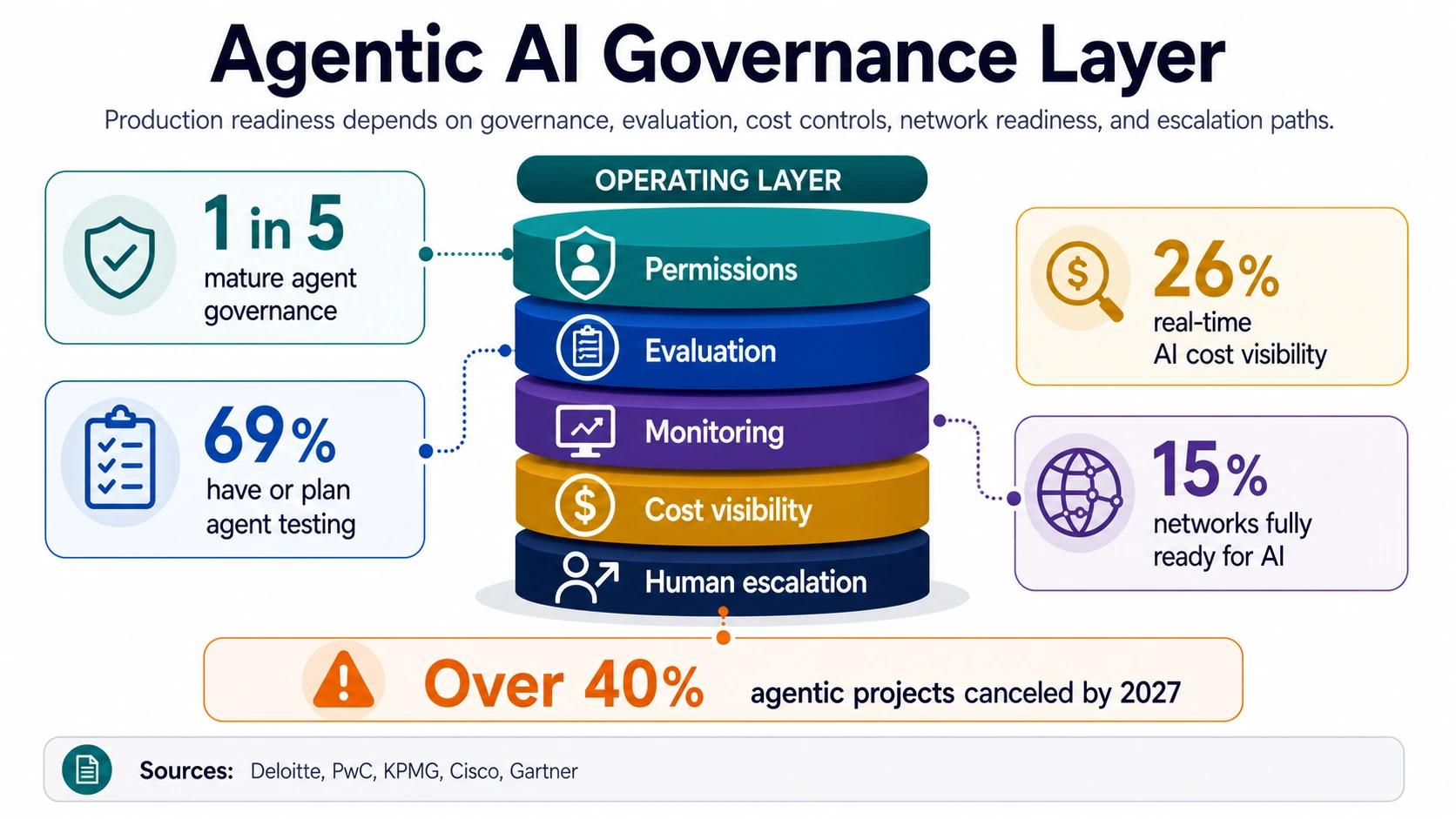

Deloitte’s finding that only one in five companies has a mature governance model for autonomous agents is the counterweight. Access can scale through licenses. Transformation requires new roles, permission models, monitoring, escalation paths, and accountability for decisions made with or by AI systems.

Production Deployment And ROI Signals Are Mixed

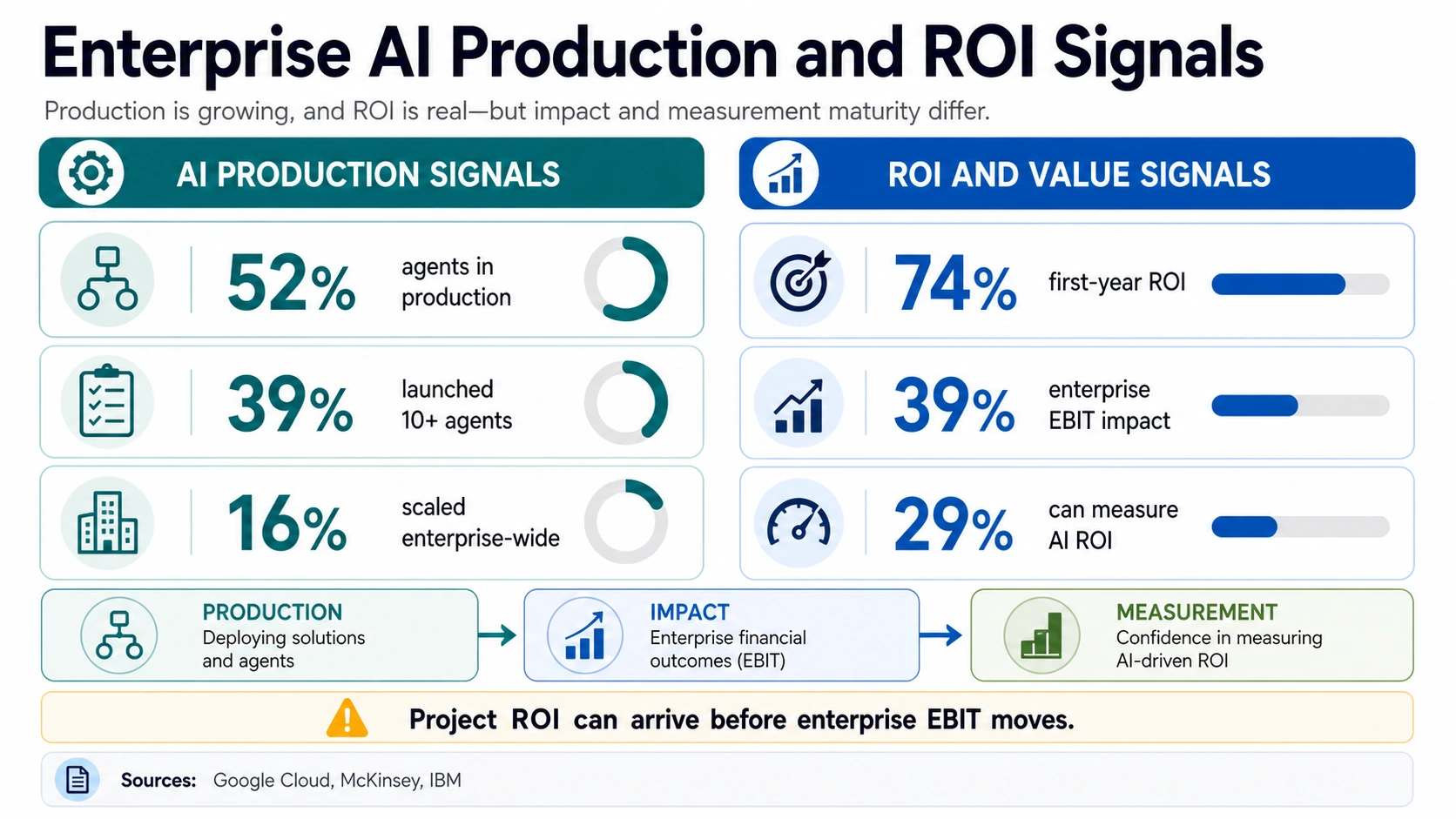

The strongest positive ROI signal comes from organizations that have moved beyond experimentation. Google Cloud’s global executive survey found that 74% of organizations using generative AI achieved ROI within the first year. Its agent-focused release also found that 52% of executives said their organizations had deployed AI agents in production, 39% had launched more than 10 agents, and 56% reported business growth from generative AI.

Those figures should be read with the sample in mind. The Google Cloud survey focuses on senior leaders at enterprises with generative AI deployment. It is useful for understanding what AI-active enterprises are seeing, not for estimating adoption across all businesses. Within that group, productivity, customer experience, business growth, and faster deployment cycles are recurring outcomes.

McKinsey’s survey gives a more conservative ROI frame. 39% of AI-using organizations reported enterprise-level EBIT impact, but most said the impact was under 5%. That does not contradict Google Cloud’s result: ROI within a project or function can arrive before enterprise-level EBIT moves materially. In large companies, the denominator for consolidated EBIT is so large that many successful use cases stay invisible in the financials.

IBM’s synthesis focuses on measurement maturity. IBM says only about 29% of organizations can confidently measure AI ROI, even though many see productivity gains, and cites CEO-study findings that roughly one-quarter of AI initiatives deliver expected ROI and 16% scale enterprise-wide. If the baseline process, cost model, and success metric are unclear, AI impact becomes hard to defend even when teams feel faster.

The enterprise AI maturity funnel

Each stage counts a different population and comes from a different survey, so this is a narrative funnel, not one cohort tracked over time: broad use narrows to production agents, then to reported EBIT impact, then to confident ROI measurement.

McKinsey, Google Cloud, IBMThe cautionary data comes from MIT NANDA and Gartner. MIT NANDA’s preliminary business report says enterprise generative AI investment reached $30 billion to $40 billion, but 95% of reviewed initiatives delivered zero return while 5% of integrated pilots extracted millions. Gartner predicts over 40% of agentic AI projects will be canceled by the end of 2027. Both should be treated as warnings about poor fit, weak controls, unclear economics, and pilot sprawl — not proof that AI does not work.

The fairest 2026 ROI reading is neither hype nor dismissal. Enterprise AI can produce measurable value quickly in bounded use cases, especially when workflows are redesigned and metrics are explicit. Broad enterprise-level financial transformation remains less common than tool adoption.

Budgets Keep Rising Even As Leaders Demand Proof

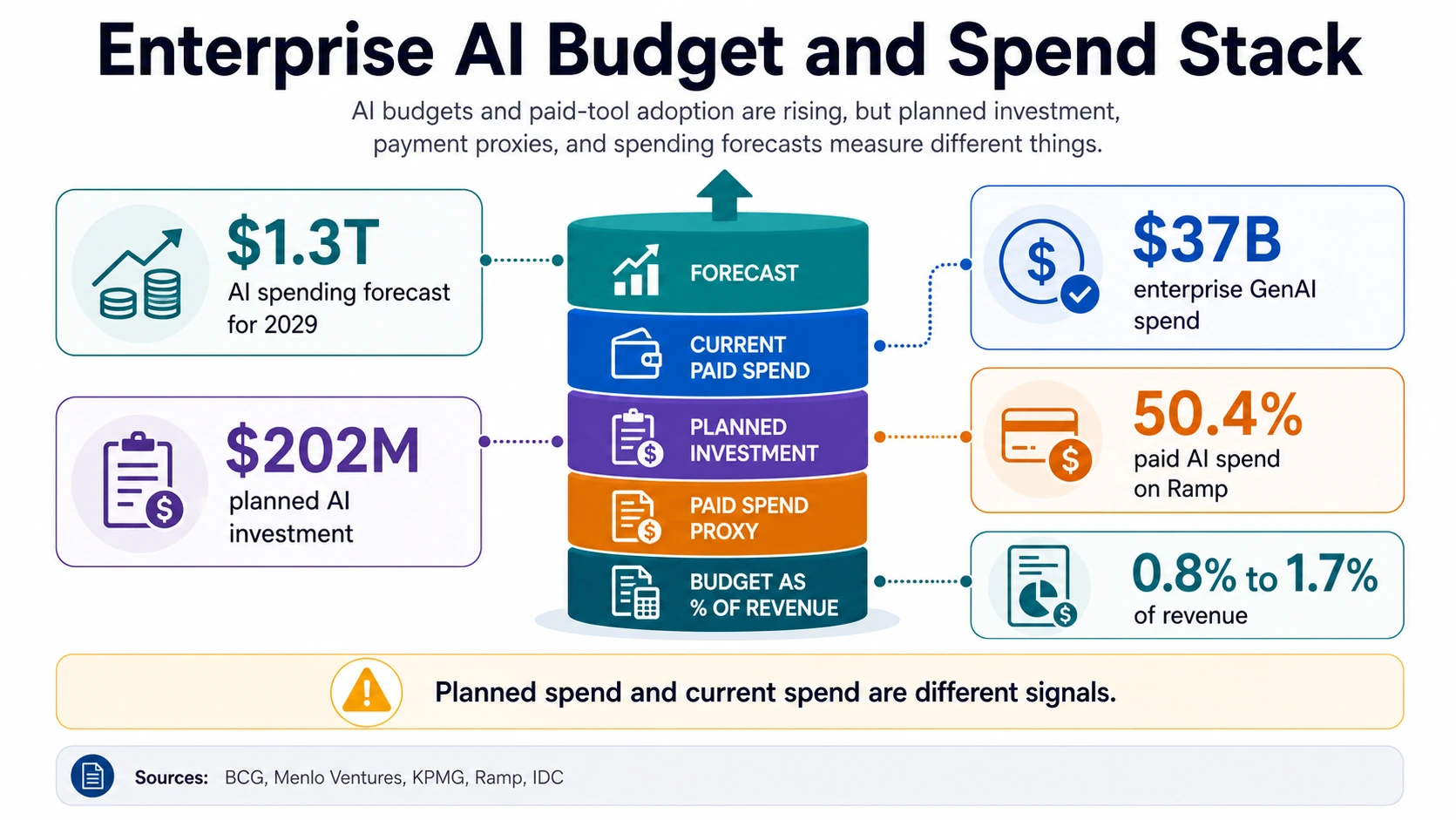

AI budgets are expanding because executives see AI as a strategic capability, not a discretionary software category. BCG’s 2026 survey says AI spending is expected to more than double from 0.8% to 1.7% of revenue, and 94% of surveyed executives said they would keep investing even if returns did not arrive in 2026. Leaders are treating AI as a multi-year operating shift rather than a quarterly ROI experiment.

Menlo Ventures estimates that enterprise generative AI spend reached $37 billion in 2025, up 3.2 times from $11.5 billion in 2024, with $19 billion going to the application layer. Enterprises are no longer only buying foundation-model access. They are buying applications, workflow tools, coding assistants, sales and service systems, data platforms, and automation layers that package models into daily work.

IDC worldwide AI spending forecast

IDC projects a 31.9% compound annual growth rate from 2025 to 2029, reaching $1.3 trillion. Points between endpoints are a smooth CAGR interpolation, shown for shape only. Source: IDC.

KPMG’s Q2 AI Pulse found that leaders planned an average of $202 million in AI investment over the next 12 months, but only 26% had real-time visibility into AI costs and 35% cited cost management or economic literacy as a barrier. In Q4, KPMG reported planned AI spending of $124 million over the next year, with 67% saying they would maintain AI spending even in a recession. The lower Q4 figure does not erase the trend; it shows leaders revising programs as agent and model costs become more visible.

Ramp’s payment-based data shows AI spending becoming routine across business segments. Its March 2026 AI Index reached 50.4%, with much higher adoption among venture-backed and private-equity-backed firms. Procurement can reveal adoption that surveys miss: a company may not describe itself as an AI adopter, but recurring invoices for AI products show AI entering the software stack.

IDC’s forecast gives the macro version of the same trend. Worldwide AI spending is projected to reach $1.3 trillion in 2029, growing at a 31.9% compound annual rate from 2025. Gartner expects 40% of enterprise applications to feature task-specific AI agents by the end of 2026, up from less than 5% in 2025. If that holds, much adoption will arrive through software upgrades rather than standalone AI projects. Accenture’s disclosures show the service-market side: $2.7 billion in generative and agentic AI revenue in fiscal 2025 and $5.9 billion in related bookings.

Where Enterprises Are Deploying AI First

Enterprise AI adoption is concentrated in functions with high-volume language work, customer interaction, analysis, content, software, and repeatable decisions. McKinsey reports common AI activity in IT, marketing and sales, service operations, and knowledge management. These functions share a practical trait: much of the work can be accelerated by search, summarization, classification, drafting, coding, routing, or decision support.

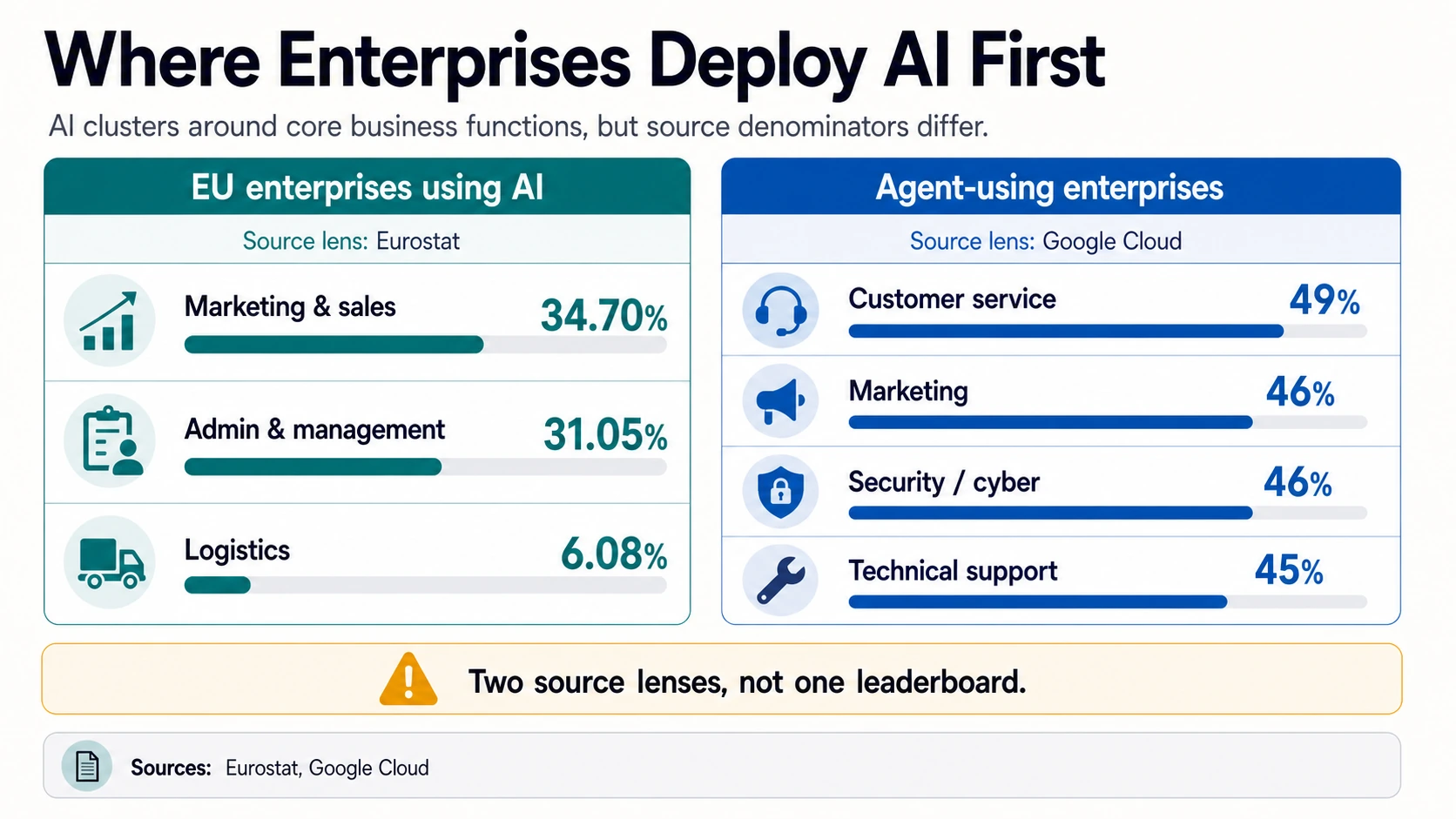

Eurostat gives a more official breakdown for EU companies using AI. Among enterprises using AI, 34.70% used it for marketing or sales, 31.05% for business administration or management, and 6.08% for logistics. By technology, 11.75% of all EU enterprises used text mining, 9.55% used image, video, audio, or text generation, and 8.76% used language or code generation — rising to 31.68% in large enterprises.

Two source lenses, not one leaderboard

These use-case rankings come from different denominators — do not merge them. Tap to switch between Eurostat's EU-enterprise purposes and Google Cloud's agent-using enterprises.

Eurostat, Google CloudCustomer service is one of the clearest agent adoption areas. Google Cloud reports that among agent-using organizations, customer service or experience was the most common use case at 49%, followed by marketing at 46%, security and cyber at 46%, and technical support at 45%. Salesforce reports that 85% of service organizations use at least one form of AI, and Zendesk says CX leaders increasingly see memory-rich AI agents as central to personalized journeys.

Software development remains a high-adoption internal use case even when it is not counted as a separate AI program. Eurostat’s 8.76% language or code generation figure across all EU enterprises rises sharply among large enterprises, and McKinsey puts IT among the most common AI use areas. Code generation, code explanation, test writing, documentation, and issue triage map well to the strengths of generative models. Security and cyber use cases are also moving into production, with Google Cloud listing security and cyber at 46% among agent use cases.

Administrative and management work is the sleeper category. Asana found 25% of knowledge employees using AI for administrative tasks, and Eurostat found 31.05% of AI-using EU enterprises applying AI to business administration or management. This is where internal copilots, meeting summaries, document drafting, spreadsheet analysis, and workflow automation create many small gains that rarely show up as a single headline project.

Agentic AI Is Moving Fast, But Governance Is The Brake

Agentic AI adoption is the most confusing part of the 2026 landscape because definitions vary. McKinsey reports that 23% of organizations were scaling agentic AI somewhere, while 39% were experimenting. Google Cloud reports 52% production agent deployment among executives at enterprises with generative AI. KPMG’s Q2 pulse found 53% deploying agents, while its Q4 update found 26% agent deployment after a Q3 peak of 42%.

These numbers coexist because “agent” can mean several things: a customer-service assistant with tool access, a workflow bot that completes multi-step tasks, a coding agent, a security triage assistant, an internal research assistant, or a group of agents coordinated around a business process. A narrow, tool-using assistant is far easier to deploy than a high-autonomy system that can execute transactions, change records, or trigger downstream actions.

Governance maturity is the constraining factor. Deloitte says only one in five companies has a mature governance model for autonomous agents. PwC found that 69% of strategic-stage organizations have or plan evaluation and testing for AI agent activity. KPMG says only 26% have real-time AI cost visibility — which matters because autonomous and semi-autonomous systems can create usage costs that are hard to manage after deployment.

The control problem is not abstract. OWASP describes excessive agency as a risk when LLM-based systems are given too much functionality, permission, or autonomy. NIST’s Generative AI Profile recommends structured validation, purpose-built testing environments, documented limitations, source and citation review, and post-deployment monitoring plans. These controls are what let a company move from a helpful assistant to a trusted workflow actor.

Governance, Regulation, And Infrastructure Are Now Adoption Issues

AI governance has moved from legal review to operational readiness. The NIST AI Risk Management Framework was created to help organizations manage AI risks to individuals, organizations, and society. For enterprise adoption, the important point is not only compliance but repeatability: teams need a shared way to map risks, measure performance, define human oversight, document limitations, and monitor systems after release.

Regulation is another reason adoption differs by market and use case. The EU AI Act entered into force on August 1, 2024, with obligations becoming applicable in phases, including full applicability from August 2, 2026, subject to exceptions and later timelines for some high-risk areas. Enterprises operating across borders need to classify systems, manage documentation, train staff, and understand when general-purpose or high-risk requirements apply.

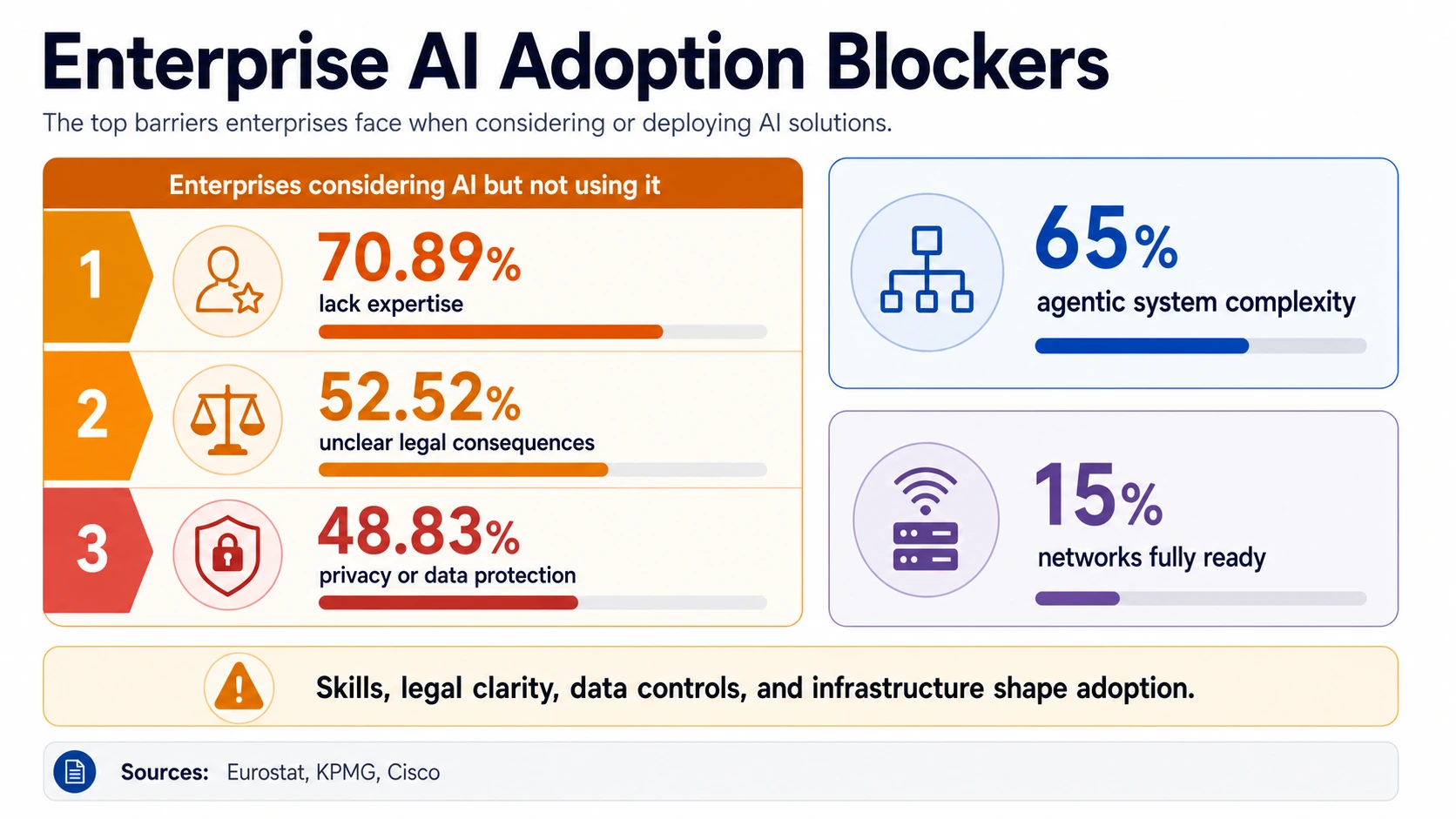

Infrastructure readiness can also slow adoption. Cisco reports that 58% of organizations have a well-defined AI strategy, but only 15% have networks fully ready for AI. Production AI is data-hungry, latency-sensitive, security-sensitive, and often integrated into many existing systems. A strategy deck cannot compensate for weak data access, brittle identity controls, poor observability, or overloaded networks.

Cost governance is increasingly visible. KPMG’s Q2 AI Pulse found that only 26% of leaders had real-time visibility into AI costs, while 66% used dashboards, 61% used approval processes, and 36% used direct token or usage controls. AI costs are not always shaped like traditional SaaS seats: usage-based models, agent loops, retrieval calls, model tiers, and vendor-specific pricing can turn a successful pilot into a budget surprise. Data privacy and security remain core buying criteria — Google Cloud reports that 37% of executives ranked data privacy and security among their top three considerations when choosing an LLM provider, and Eurostat found 48.83% of EU non-adopters citing privacy or data protection concerns.

The Biggest Blockers Are Skills, Legal Clarity, Data, And Change Management

The leading AI adoption blockers are remarkably consistent across datasets. Eurostat’s official enterprise survey found that among enterprises that considered AI but did not use it, 70.89% cited lack of expertise. That is the single most direct explanation for why small and medium enterprises lag large ones: a firm may see the value but lack the people to evaluate, implement, integrate, and monitor the system.

Legal uncertainty is the second major blocker. Eurostat reports 52.52% citing unclear legal consequences, and the EU AI Act adds a phased compliance environment for companies operating in Europe. Legal uncertainty can slow procurement, data sharing, model selection, use-case approval, and deployment into customer-facing workflows.

Complexity is rising as enterprises move from copilots to agents. KPMG’s Q4 AI Pulse found that 65% cited agentic system complexity as a top barrier. Agent systems touch more of the business than prompt-response tools — they need tool permissions, workflow integration, evaluation, cost limits, handoffs, monitoring, and a human operating model that defines who owns the agent’s work.

Skills and incentives show up in workforce research too. Microsoft found that only 13% of AI users felt rewarded for reinvention, while many feared falling behind. Enterprise AI adoption is not only a training problem; it is also a management problem, where people need permission, role clarity, and a reason to redesign the job rather than privately speeding up old tasks. Data and infrastructure constraints remain stubborn: Cisco’s 15% network-readiness figure is a reminder that AI adoption depends on technical foundations outside the model layer.

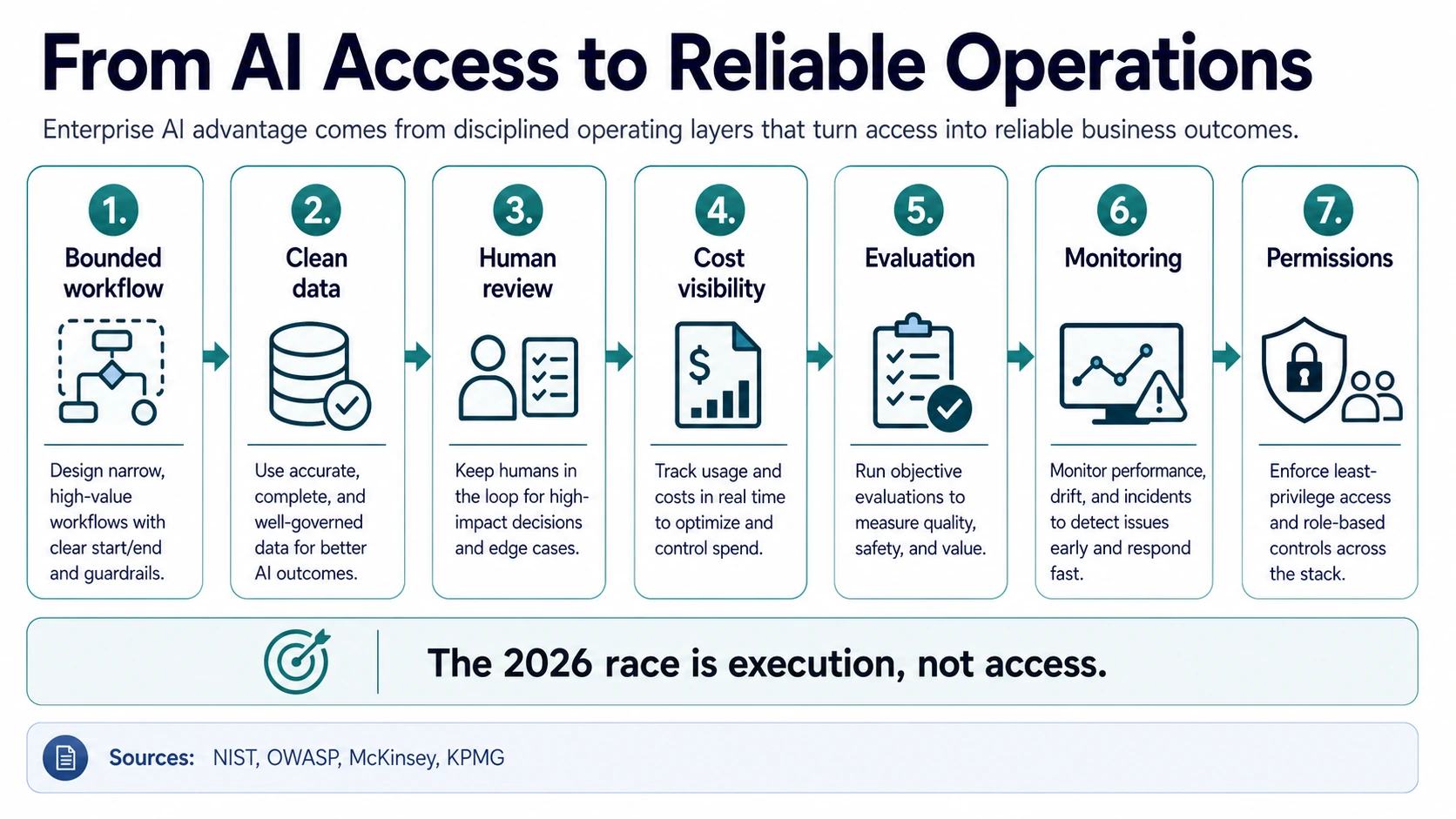

What The 2026 Data Means For Operators And AI Builders

For enterprise operators, the adoption data argues for narrowing the first production workflows. The strongest early use cases usually have a defined work queue, measurable cycle time, known quality criteria, and a clear human reviewer. Customer support triage, sales research, marketing production, coding assistance, compliance review, procurement analysis, and internal knowledge work all fit this pattern — narrow enough to measure and important enough to matter.

Start with a bounded workflow.

Pick a defined work queue with measurable cycle time, known quality criteria, and a clear human reviewer before scaling.

Fix the data foundation.

Clean internal data, secure connectors, identity-aware access, and retrieval quality — Cisco found only 15% of networks fully ready for AI.

Keep a human in the loop.

Assign, check, and combine AI outputs with explicit accountability; transformation needs new roles, not just licenses.

Make cost visible.

Only 26% of leaders have real-time AI cost visibility (KPMG); usage-based models and agent loops can turn a pilot into a budget surprise.

Build evaluation in.

PwC found 69% of strategic-stage organizations have or plan evaluation and testing for agent activity — build it before launch, not after.

Plan post-deployment monitoring.

NIST recommends structured validation, documented limitations, and monitoring plans as standing practice, not paperwork.

Scope permissions tightly.

OWASP warns that excessive agency — too much functionality, permission, or autonomy — is a core LLM risk to design against.

For AI builders, the opportunity is no longer just model access. Buyers need deployment maturity: security controls, admin visibility, usage analytics, workflow integration, evaluation harnesses, audit logs, data controls, role-based permissions, and credible ROI claims. McKinsey’s evidence that high performers are more likely to redesign workflows should shape product design — tools that fit the real workflow beat tools that only demo well.

The budget data is encouraging but raises the bar. BCG’s expected AI spend increase to 1.7% of revenue, Menlo’s $37 billion enterprise GenAI spend estimate, and IDC’s $1.3 trillion 2029 forecast all point to a large market. KPMG’s 26% real-time cost visibility figure points to the next buyer concern: vendors that help customers see cost, quality, and risk in one place will have a stronger enterprise case. For teams adopting AI internally, the safest path is staged — assistive workflows first, then bounded automation, then agentic action where the risk is known and the review loop is strong.

Reading Adoption Data Without Getting Misled

When a statistic says “AI adoption,” check the denominator first. A large-enterprise executive survey like McKinsey’s 88% AI use measures organizational exposure among surveyed respondents. An official business survey like Eurostat’s 19.95% enterprise AI use measures a broader population. A workforce survey like Gallup’s 50% employee AI use measures individual behavior. A spend index like Ramp’s 50.4% AI payment adoption measures vendor payments. Each is valid, but none should be used alone.

Then check the maturity level. Exploration, paid license, pilot, production deployment, scaled deployment, measured ROI, and enterprise EBIT impact are different stages. The MIT NANDA report’s gap between widespread exploration and 5% custom-tool production is one way to see the maturity issue. Deloitte’s gap between 50% access growth and 34% true business reimagination is another.

Finally, check whether the system is assistive or autonomous. A writing assistant, an internal search copilot, a code suggestion tool, and an agent that can call tools and change records all carry different risk. Gartner’s agent cancellation forecast, Deloitte’s one-in-five mature agent governance figure, and PwC’s agent evaluation and testing signal all show why agent statistics require extra caution.

Frequently Asked Questions

What percentage of companies use AI in 2026?

It depends on the denominator. McKinsey found 88% of surveyed organizations regularly use AI in at least one function, and the Stanford AI Index reports 88% organizational adoption. But official business surveys are far lower: the U.S. Federal Reserve estimates about 18% of firms had adopted AI by the end of 2025, and Eurostat reports 19.95% of EU enterprises used AI in 2025.

Why do enterprise AI adoption statistics vary so much?

Because each survey counts a different population. Executive surveys like McKinsey (88%) sample AI-forward organizations, official statistics agencies like Eurostat (19.95%) count every firm including small ones, employee surveys like Gallup (50%) measure individual behavior, and payment indices like Ramp (50.4%) measure vendor spend. All are valid, but none should be used alone.

How many enterprises have deployed AI agents in production?

Estimates diverge by sample and definition. Google Cloud found 52% of executives at generative-AI enterprises said their organizations deployed agents in production, and KPMG Q2 found 53% deploying agents — but KPMG Q4 reported just 26%, down from 42% in Q3. Gartner predicts over 40% of agentic AI projects will be canceled by the end of 2027.

Can companies actually measure ROI from AI?

Often not confidently. Google Cloud reports 74% of organizations using generative AI achieved ROI within the first year, but IBM says only about 29% can confidently measure AI ROI. McKinsey found 39% of AI-using organizations report enterprise-level EBIT impact, though most say the impact is under 5%.

How much are enterprises spending on AI?

Menlo Ventures estimates enterprise generative AI spend reached $37 billion in 2025, up from $11.5 billion in 2024. BCG expects AI spending to more than double from 0.8% to 1.7% of revenue, and IDC forecasts worldwide AI spending will reach $1.3 trillion in 2029, growing at a 31.9% compound annual rate from 2025.

What are the biggest blockers to enterprise AI adoption?

Eurostat found that among EU enterprises that considered AI but did not adopt it, 70.89% cited lack of expertise, 52.52% cited unclear legal consequences, and 48.83% cited privacy or data protection concerns. KPMG found 65% cited agentic system complexity, and Cisco found only 15% of organizations have networks fully ready for AI.

Where are enterprises deploying AI first?

In high-volume language and customer functions. Among EU enterprises using AI, Eurostat found 34.70% use it for marketing or sales and 31.05% for business administration. Among agent-using organizations, Google Cloud found customer service or experience was the top use case at 49%, followed by marketing at 46%, security and cyber at 46%, and technical support at 45%.

Is AI use spreading faster than organizations can adapt?

Yes. Deloitte found employee AI access rose 50% in 2025 but only 34% of organizations are truly reimagining the business, and Microsoft found only 26% of AI users said leadership was aligned while just 13% felt rewarded for reinvention. Access is spreading faster than operating-model change.

Sources and Further Reading

Executive & management surveys

Official statistics & workforce data

Spend, forecasts & market context

Governance, regulation & use cases