AI Agent Adoption Statistics

Last updated on July 6, 2026

AI agents are moving from demo videos into real workflows, but the adoption numbers only make sense if you keep the definitions straight. In 2026, a company can be “using AI” because employees write with ChatGPT, “adopting agents” because a team is piloting a tool-connected workflow, “deploying agents in production” because customer support or sales ops uses them with guardrails, or “scaling agentic AI” because multiple functions are redesigning work around delegated action.

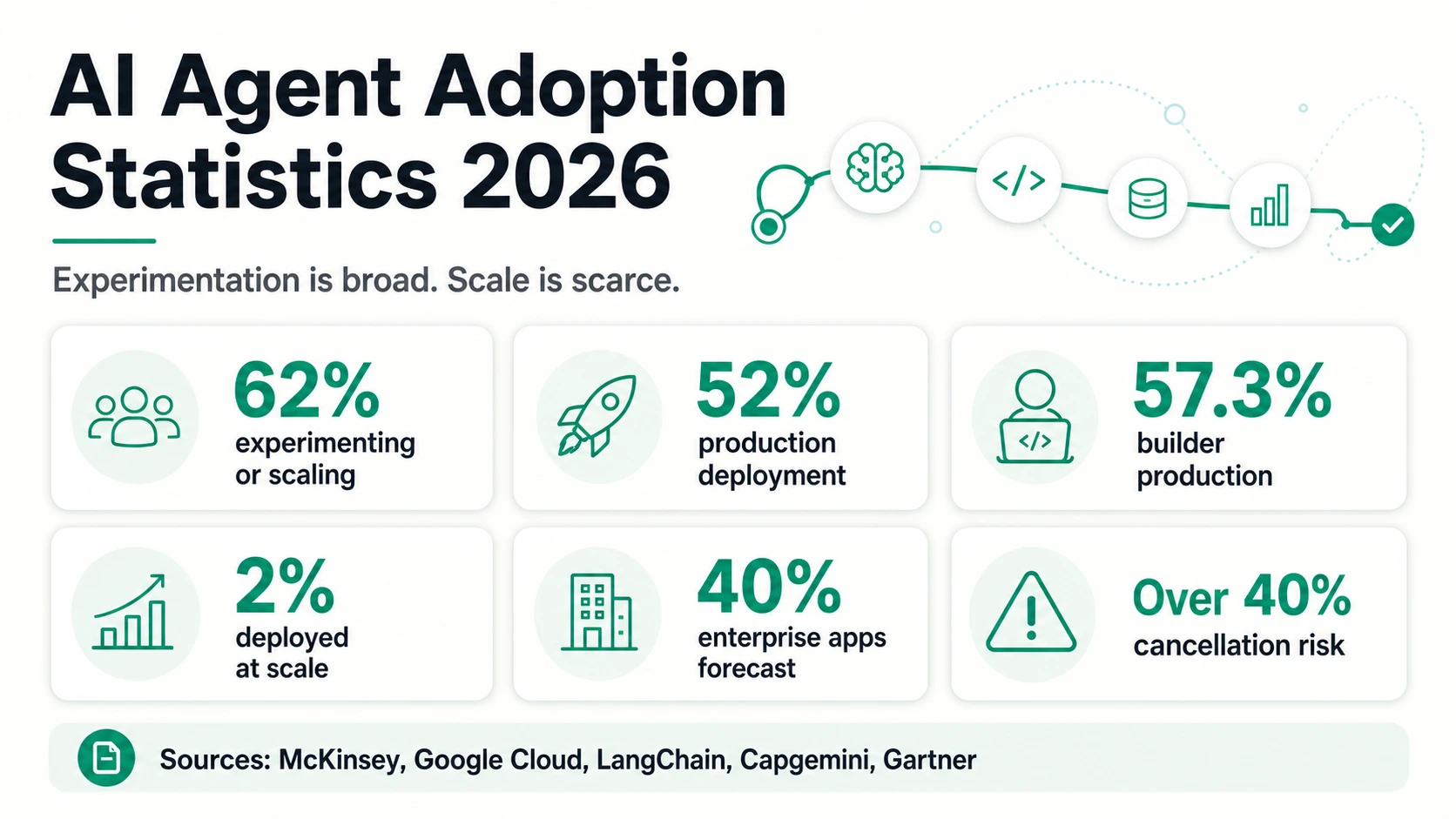

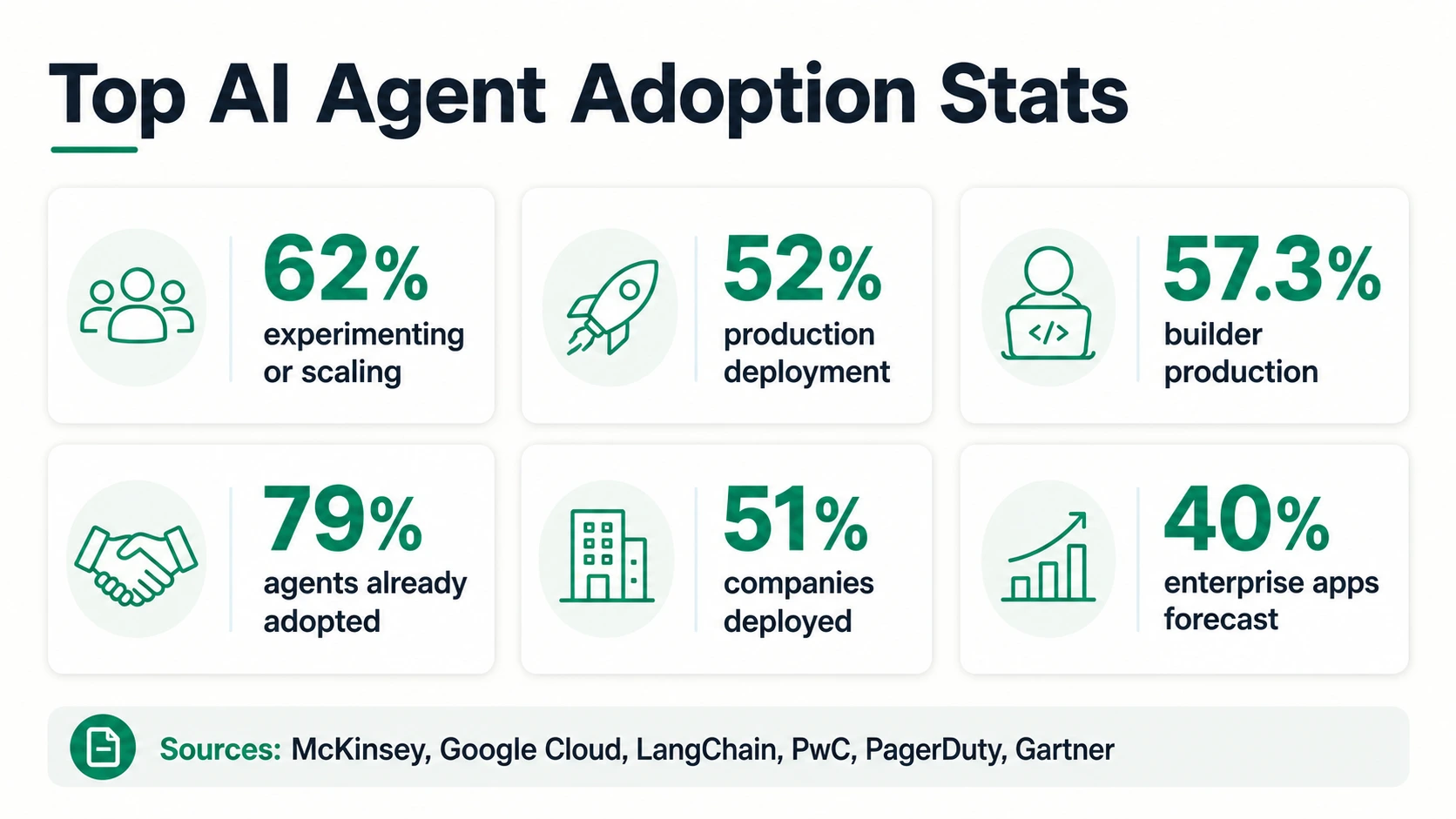

That distinction is the whole story. McKinsey reports that 62% of survey respondents are at least experimenting with AI agents, while Google Cloud says 52% of executives at organizations already using gen AI report production AI-agent deployment, and LangChain’s builder-heavy survey finds 57.3% with agents in production. Those numbers point in the same direction: agent adoption is real. But Capgemini’s breakdown, with only 2% deployed at scale and 12% at partial scale, shows why “real” does not mean “fully mature.”

AI Agent Adoption, By The Numbers

The headline AI-agent numbers look high, but they measure different layers of adoption — experimentation, self-reported deployment, builder-sample production, and forecast — so read them as separate signals rather than one figure.

Adoption & deployment (survey headlines)

Maturity, forecasts & risk

Read every number by its own denominator

AI-agent statistics answer different questions depending on the population and the maturity word. Tap a metric to see what it measures — and what it does not prove.

McKinsey, Google Cloud, LangChain, CapgeminiWhich Numbers Actually Mean “Adoption”

An AI agent is not just a chatbot with a new label. IBM defines an AI agent as a system that autonomously performs tasks by designing workflows with available tools. AWS describes an AI agent as software that interacts with its environment, collects data, and performs self-directed tasks toward goals set by humans. Google Cloud says agents pursue goals, complete tasks on behalf of users, and show reasoning, planning, memory, and autonomy. OpenAI’s Agents SDK documentation describes agents as applications that plan, call tools, collaborate across specialists, and keep enough state to complete multi-step work.

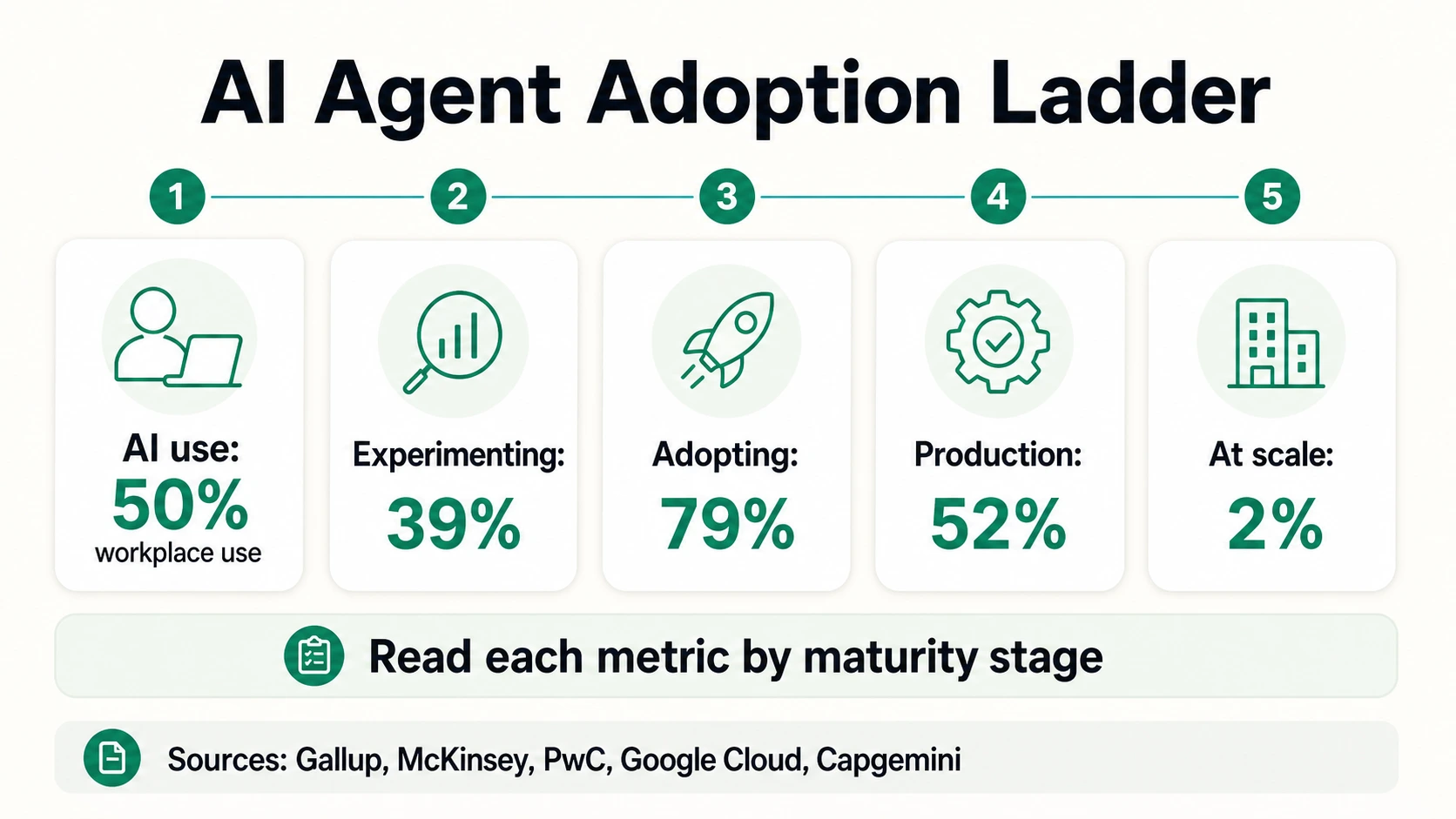

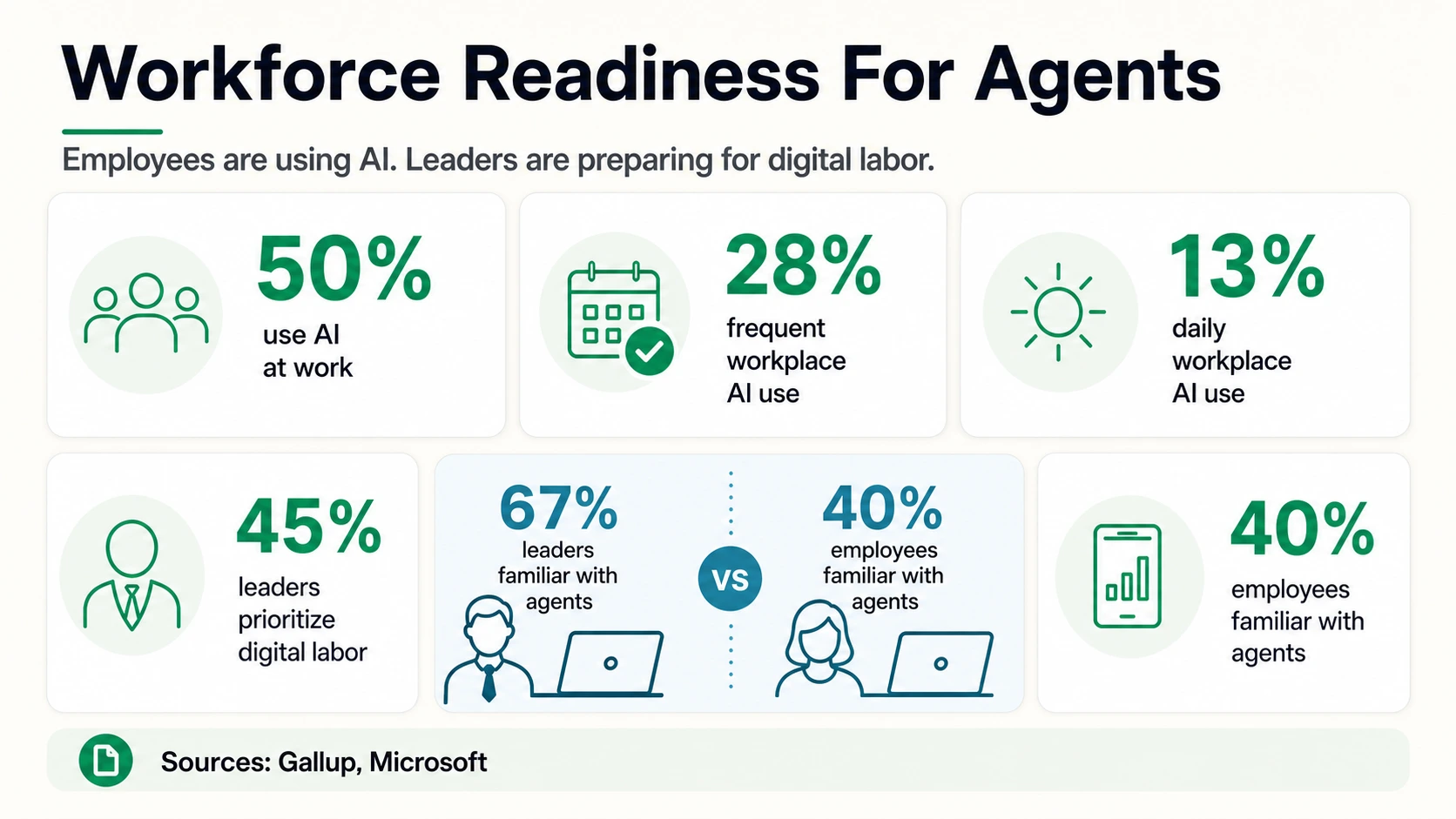

Those definitions share a few practical ingredients: the agent has a goal, access to tools or systems, some ability to plan or choose next steps, and a boundary around what it can do. That is why general AI use and agent adoption should not be merged. Gallup’s 50% workplace AI-use figure is useful because it shows employee readiness, but it does not mean half of U.S. employees are using autonomous agents. Stanford HAI’s 2026 AI Index says generative AI reached 53% population adoption within three years, but that is a broad gen-AI adoption statistic, not an enterprise-agent deployment rate.

General AI use

Employees use AI for writing, summarizing, coding, research, or analysis — the Gallup and Asana readiness layer.

Agent experimentation

A team tests a tool-connected system, matching McKinsey's 39% experimentation bucket.

Agent adoption

A company says agents are being adopted, as in PwC's 79% adoption figure.

Production deployment

An agent runs in live internal or customer-facing workflows — Google Cloud's 52%, PagerDuty's 51%, LangChain's 57.3%.

Scaling

Agentic systems expand across a function or multiple workflows — McKinsey's 23% and Capgemini's partial-scale and at-scale buckets.

Autonomous action with governance

Agents act inside systems with permissions, auditability, evaluation, and human handoffs — the OWASP and NIST risk area.

This ladder matters because AI-agent statistics often sound more mature than the underlying workflow. A broad survey can capture interest, pilots, or adoption language, while an engineering survey can capture real production systems among teams that are unusually close to the tooling. Neither view is wrong, but each answers a different question. The market-sizing question is “How many organizations are planning around agents?” The operations question is “Which workflows already let an agent act, log what happened, and recover safely when the answer is uncertain?” The second question is narrower, but it is the one that determines whether adoption creates durable productivity.

For a buyer, the most useful adoption signal is usually not the highest percentage. It is the most specific verb. “Using” can mean an employee prompts a model. “Testing” can mean a controlled pilot. “Deploying” should mean the agent is available in a live workflow. “Scaling” should mean more than one team, process, or business unit depends on it. When those verbs are separated, the 2026 picture becomes less contradictory: interest is broad, production is visible in AI-active organizations, and true scale is still scarce.

Enterprise Adoption: Experiments Are Common, Scale Is Scarcer

The adoption story is strongest when the numbers are read together. McKinsey’s survey shows 62% of respondents are at least experimenting with agents, which is a broad signal of market interest. But the same McKinsey page says no individual business function has more than 10% of respondents reporting scaled AI-agent use. That is the difference between “the enterprise is interested” and “the enterprise has reorganized around agents.”

Google Cloud’s 52% production statistic is more mature, but it comes from executives whose organizations are already using gen AI. That makes it an important production benchmark for AI-active organizations, not a universal market penetration rate. PagerDuty’s 51% deployed figure is similar, but it is based on IT and business executives and should be read as self-reported deployment. LangChain’s 57.3% production figure is especially useful for how agents are engineered, but its respondent base is heavily technology-oriented: 63% of respondents are in technology, and 49% work at organizations with fewer than 100 people.

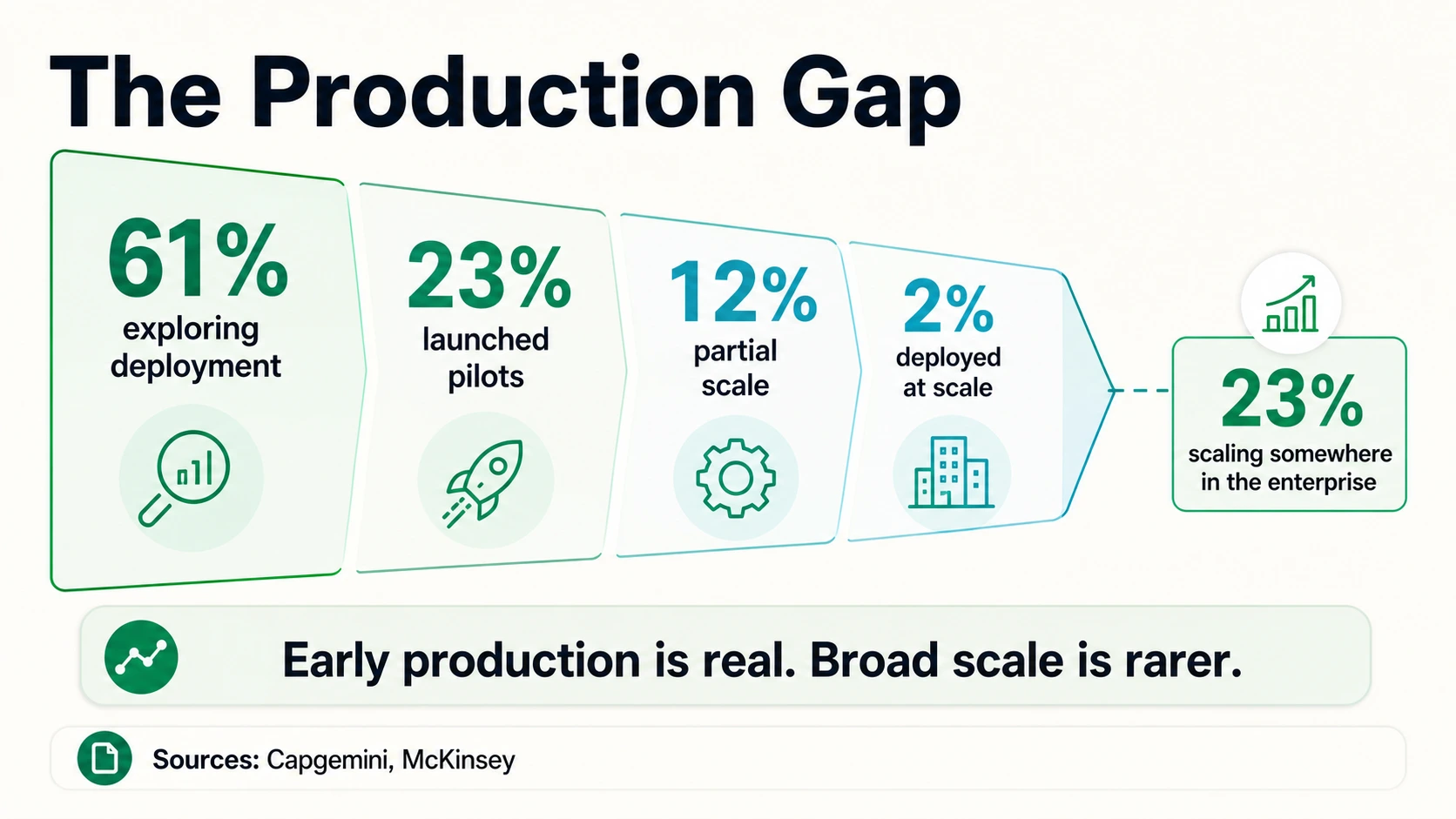

That is why Capgemini’s maturity breakdown is the helpful counterweight. A world where 61% of organizations are exploring deployment and 23% have launched pilots can still be a world where only 2% have deployed at scale. The market is not stuck at the demo stage, but it is also not uniformly operating with autonomous digital teams.

The better reading is that 2026 is the transition year from “agent as experiment” to “agent as production workflow.” KPMG’s Q4 AI Pulse Survey reported agent deployment at 26% in Q4 2025, more than double Q1’s 11%, even though the Q4 figure was lower than Q3’s 42%. KPMG says leaders are becoming stricter about what counts as a true agent and are professionalizing data, infrastructure, governance, and observability. That fits the rest of the evidence: the easy adoption is access; the hard adoption is controlled action.

KPMG agent deployment through 2025

Self-reported agent deployment across three KPMG AI Pulse quarters. The dip from 42% in Q3 to 26% in Q4 reflects a stricter bar for what counts as a true agent, not a retreat from agents.

KPMG Q4 AI Pulse SurveyThe conflict between high adoption surveys and low scale numbers is also a reminder that “enterprise” is not one market. A technology company can put an agent into a developer workflow quickly because repositories, tickets, tests, and review gates already create a structured environment. A regulated enterprise may need identity controls, data policies, vendor review, audit logs, model-risk signoff, and business-continuity planning before an agent can touch a customer record. Both companies can truthfully say they are adopting agents, but the implementation burden is not comparable.

That is why the strongest 2026 benchmark is a bundle of measures rather than a single headline. McKinsey is useful for market breadth, Google Cloud and LangChain for production momentum among AI-active groups, PagerDuty and PwC for executive appetite, Capgemini for maturity distribution, and KPMG for governance pressure. Together they show a market that has crossed the awareness threshold but has not finished the operational work.

Where AI Agents Are Being Used First

The first agent wave is not evenly distributed across every job. It is concentrating in bounded, repetitive, information-heavy workflows where an agent can retrieve data, take limited action, and escalate to a person.

Customer service is the clearest early surface. LangChain says customer service is the most common primary agent use case at 26.5%. Salesforce says customer service, internal/business automation, and sales are the top three areas for Agentforce users. Salesforce also says average daily agent-led customer-service conversations grew at an average monthly rate of 70% from January to June 2025. Those are first-mover telemetry figures, not the whole market, but they tell us where the workflows are concrete enough to measure.

Sales and internal operations are close behind. Salesforce reports drafting and sending emails, creating to-dos, sending meeting requests, querying records, summarizing records, and creating cases among common agent actions. That is important because it shows agents are not only answering questions; they are touching the operational layer. The safe pattern is usually narrow action, explicit records, clear handoff, and logs.

Research, data analysis, IT, and knowledge management are also strong early categories. LangChain puts research and data analysis at 24.4% of primary agent deployments, and internal workflow automation at 18%. McKinsey says agent use is most commonly reported in IT and knowledge management, including service-desk management and research-style workflows. For operators working with web data, this is where the connection is obvious: if a workflow involves collecting public information, extracting records, checking sources, enriching leads, monitoring pages, or updating a CRM with human approval, it is a more natural agent candidate than a vague “run my business” prompt.

Coding agents are another major adoption surface, especially among technical teams. LangChain’s write-in responses say coding agents dominate daily workflows, with tools such as Claude Code, Cursor, GitHub Copilot, Amazon Q, Windsurf, and Antigravity appearing often. That does not mean every company has production software agents, but it does show that developers are becoming comfortable with AI systems that inspect context, propose changes, call tools, and operate over multiple steps.

Human handoffs are not disappearing. Salesforce reports customer-service escalations to humans rose from 22% in Q1 2025 to 32% in Q2 2025 as agents improved routing. That is a useful correction to the simplistic “agents replace people” story. In many production workflows, a good agent reduces the low-value work and improves the moment when a human should step in.

This is also why the most credible agent deployments often look modest from the outside. A workflow that drafts a renewal email, checks a CRM field, enriches a lead list, routes a support case, or flags a page change may not sound as dramatic as an autonomous chief of staff. But it can be measured, permissioned, logged, and improved. The first wave of adoption is therefore less about replacing whole roles and more about turning repeated operational steps into monitored delegation.

Spending And Software Embedding Are Pulling Agents Into The Enterprise

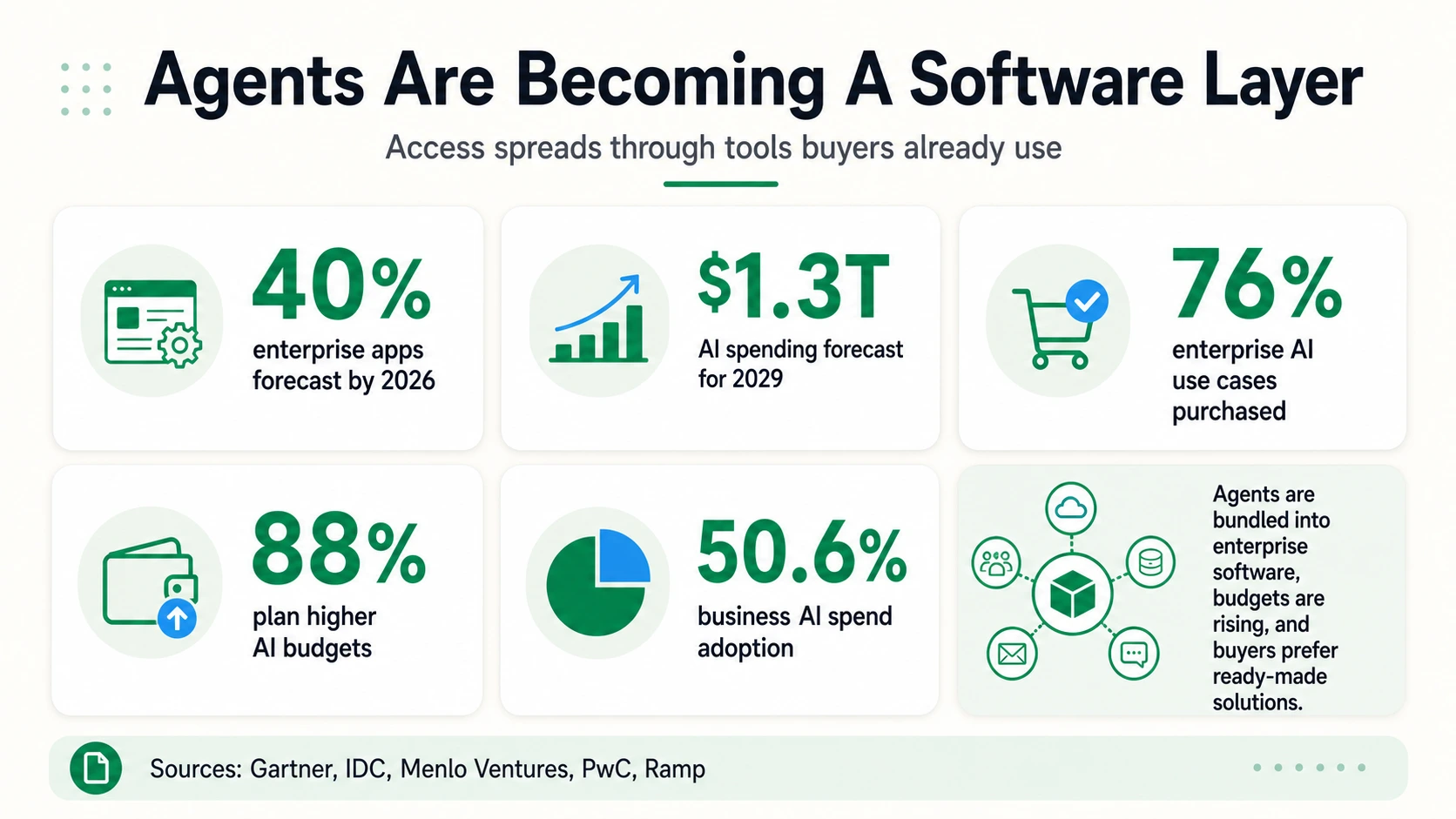

Agent adoption is not only happening through custom builds. It is also arriving through enterprise software. Gartner’s forecast that up to 40% of enterprise applications will include integrated task-specific agents by 2026 matters because many teams will first encounter agents inside tools they already use. CRM, support, finance, HR, IT service, collaboration, analytics, and ecommerce platforms can all embed narrow agents before a company has a formal agent strategy.

That can accelerate adoption and create confusion. A company might not have a homegrown agent platform, yet its support team may be using an embedded service agent, its sales team may be using an outreach agent, and its analysts may be using research assistants. Menlo Ventures says 76% of enterprise AI use cases are purchased rather than built internally, up from a roughly split build-versus-buy pattern in 2024. If that purchasing pattern carries into agents, many operators will manage a portfolio of vendor-supplied agents rather than a single internally built system.

The budget story is also strong. PwC says 88% of senior executives in its AI agent survey plan to increase AI-related budgets in the next 12 months because of agentic AI. KPMG reports 67% of leaders would maintain AI spending even if a recession occurs in the next 12 months, and 59% expect measurable ROI within that same timeframe. IDC forecasts agentic AI-enabled applications and systems to manage agentic fleets will help drive AI spending to $1.3 trillion in 2029.

Corporate AI spend data gives a related, but not agent-specific, signal. Ramp Economics Lab reported overall AI adoption at 50.6% among Ramp-measured businesses in April 2026, with Anthropic at 34.4% and OpenAI at 32.3%. That is spend-based AI adoption, not agent adoption. Still, it shows that paid AI tools have become normal enough for finance systems to measure them as a category.

The conclusion for founders is direct: access is being bundled into software, budgets are available, and buyers prefer ready-made solutions when the value is clear. The hard part is differentiation. If agents become a feature in every enterprise app, advantage moves to workflow depth, data access, permission design, observability, evaluation, and measurable outcomes.

That shift changes how agent vendors should talk about value. A buyer does not need another generic promise that an agent can “automate work.” They need to know which systems the agent connects to, what actions it can take, what data it can see, what happens when the model is uncertain, and how the organization can prove the result. Embedded agents may win distribution, but distribution alone will not settle trust. The products that stand out will package autonomy with controls: roles, scopes, approvals, traces, test sets, and clear business metrics.

It also changes internal ownership. Agent adoption touches IT, security, legal, finance, analytics, and the business function that owns the workflow. A support leader may care about handle time and escalation quality; security may care about permission boundaries; finance may care about vendor sprawl; operations may care about exception handling. The budget numbers are large because many teams see potential, but the buying committee is large because agents cross system boundaries.

The Production Gap: Why Agent Projects Stall

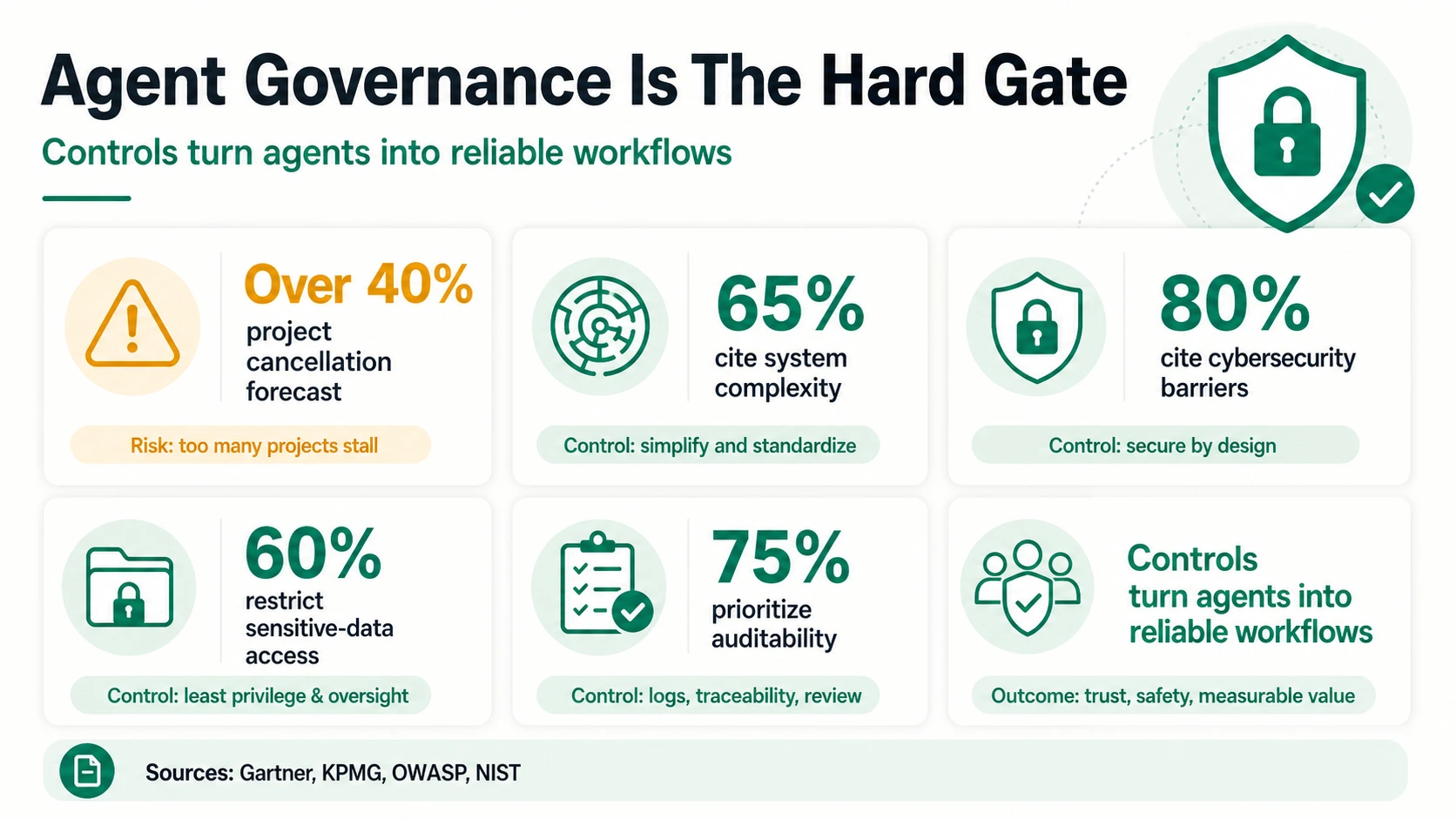

The agent market has a strange shape: high adoption intent and high failure risk at the same time. Gartner predicts over 40% of agentic AI projects will be canceled by the end of 2027, citing escalating costs, unclear business value, and inadequate risk controls. Gartner also warns that many vendors are “agent washing” older automation, assistants, RPA, or chatbots without substantial agentic capability.

Engineering data supports the same caution. LangChain says quality is the biggest production barrier, cited by 32% of respondents. Latency is second at 20%, and among larger enterprises security becomes the second-largest concern at 24.9%. These are not abstract worries. Agents take multiple steps, call tools, retrieve context, update records, and sometimes communicate with customers. Each step is a new place for the system to be wrong, slow, over-permissioned, or hard to audit.

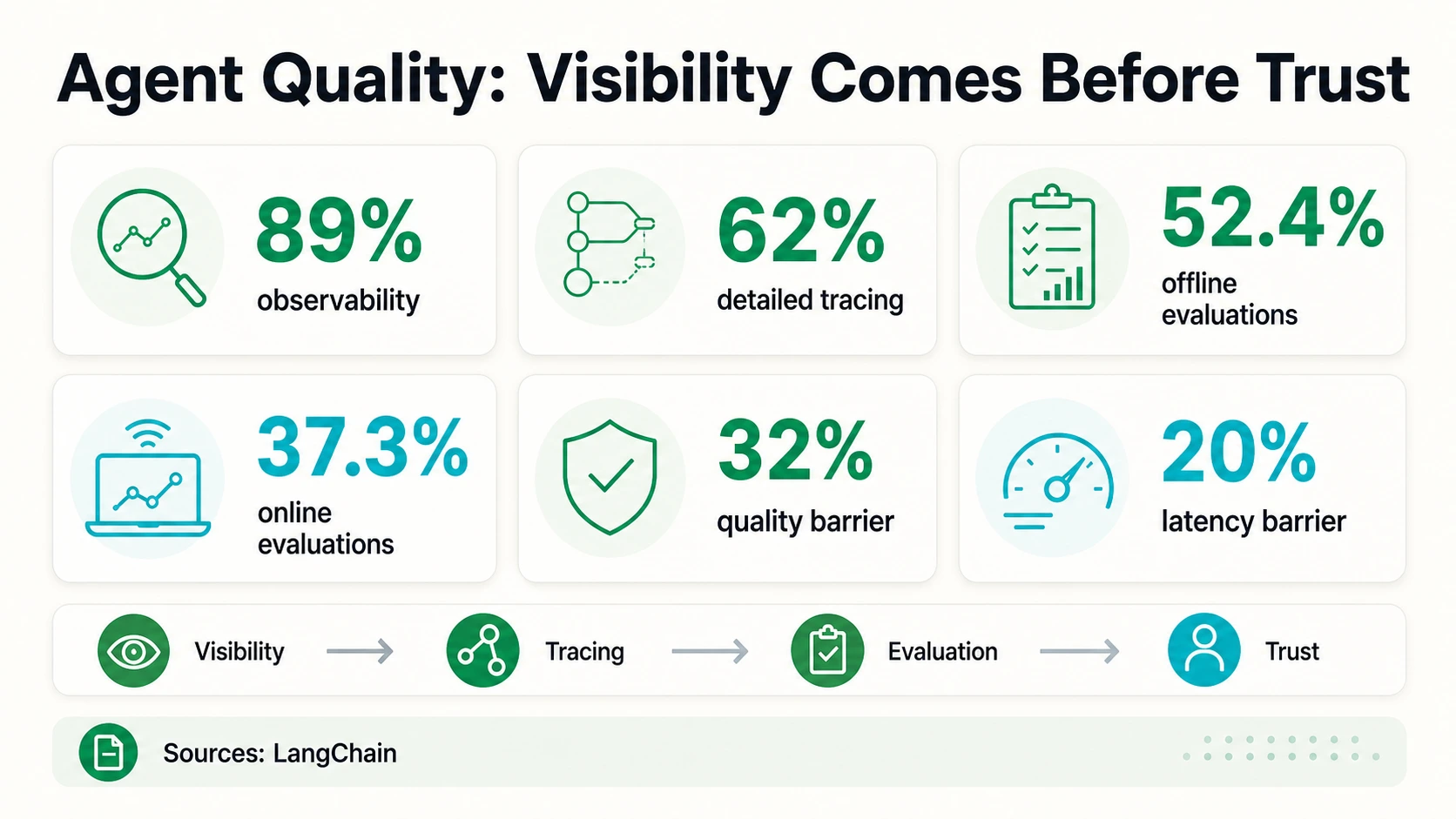

The observability and evaluation gap is especially revealing. LangChain says 89% of organizations have some observability for agents, and 62% have detailed tracing. But only 52.4% run offline evaluations, and 37.3% run online evaluations. In plain English: more teams can see what their agents did than can systematically prove that their agents are good enough.

Security frameworks explain why this matters. OWASP’s 2025 Excessive Agency category says LLM-based systems can be risky when they have excessive functionality, excessive permissions, or excessive autonomy. OWASP’s examples include agents with unnecessary delete/write capabilities, generic privileged identities, open-ended extensions, and high-impact actions without independent confirmation. NIST’s AI Risk Management Framework and NIST AI 600-1 Generative AI Profile provide broader risk-management guidance for organizations trying to align AI behavior with governance, security, privacy, and accountability.

The work-design problem is just as important as the model problem. MIT NANDA’s 2025 State of AI in Business report says many enterprise gen-AI systems fail because of brittle workflows, lack of contextual learning, and misalignment with daily operations. That report is about gen AI broadly, not agents alone, so it should not be used as an agent-specific failure rate. But it explains the pattern seen in agent adoption: generic AI tools spread quickly, while integrated systems require process redesign.

Asana’s 2025 State of AI at Work makes the same point in more operational language: AI becomes another layer of complexity when it is bolted onto broken systems, while “AI Scalers” redesign work around AI. Gallup also finds that 65% of employees in AI-adopting organizations say AI has improved productivity, but few say AI has fundamentally transformed how work gets done. Agents magnify that gap because they do not merely assist; they act.

The common failure mode is not that the model cannot produce a plausible answer. It is that the surrounding workflow is not ready for delegated action. The agent may lack the right context, use stale data, call the wrong tool, overstep a permission boundary, fail to ask for approval, or complete a task that cannot be audited later. In a chat-only assistant, those errors may be annoying. In a tool-connected agent, they can create customer-facing mistakes, bad records, duplicate work, or security incidents.

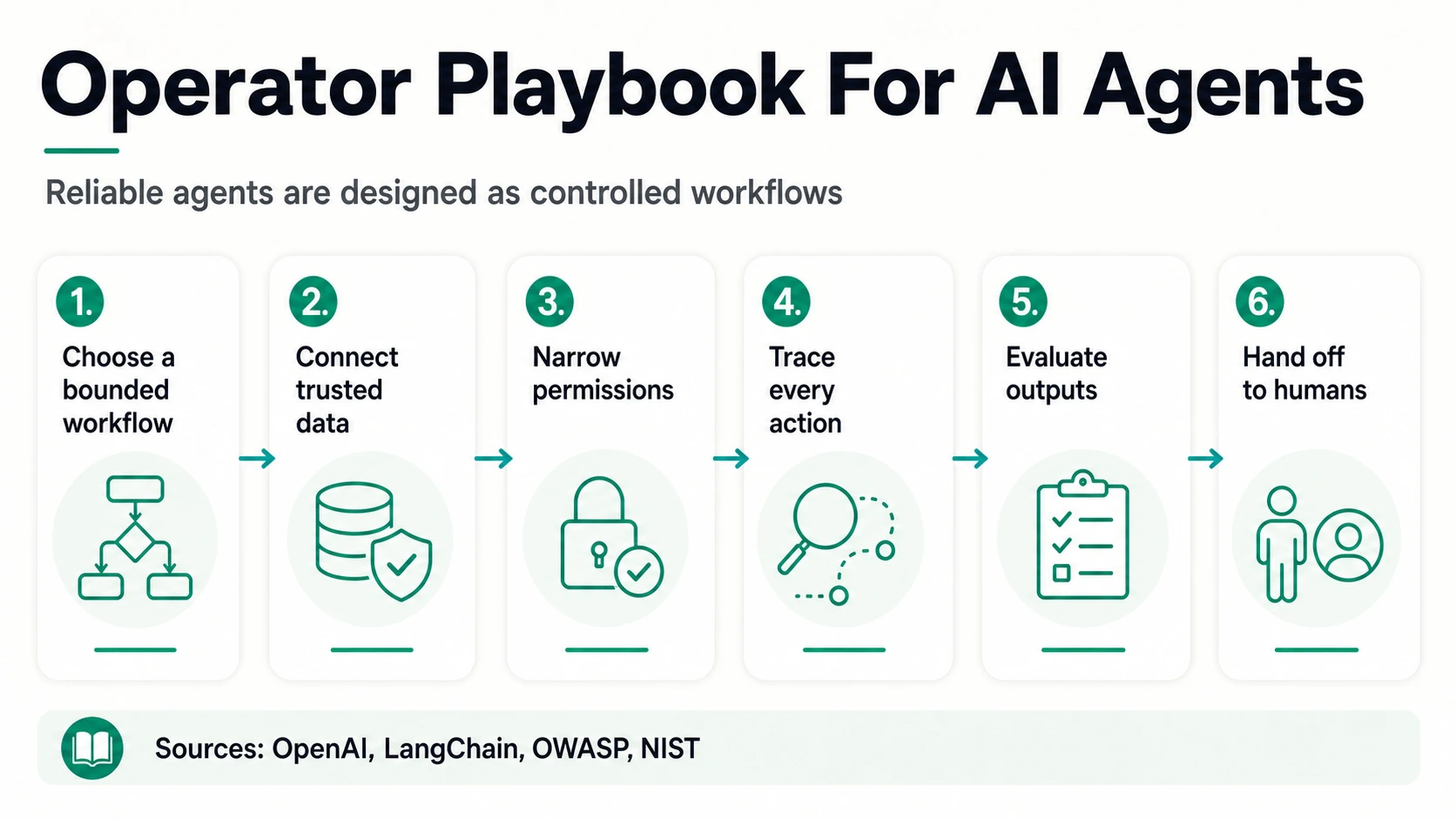

Production teams therefore need measurement before scale. A useful agent program should define acceptable tasks, expected inputs, disallowed actions, escalation triggers, and success criteria before expanding the workflow. Offline evaluations can test whether an agent handles known scenarios. Online evaluations can monitor live drift. Tracing can show which tools were called and why. Human review can catch high-impact actions. These practices are not bureaucratic extras; they are what turn a promising demo into a system a business can trust.

The Operator’s Read On Agent Adoption

The first implication is that agent adoption should be sold and managed as workflow delegation, not as model access. The market already has access. Stanford HAI’s 53% population-level gen-AI adoption figure, Gallup’s 50% U.S. workplace AI-use figure, and Ramp’s 50.6% business AI spend adoption figure all point to a world where AI usage is normalizing. What is scarce is reliable delegated work inside real systems.

The second implication is that “agent adoption” is too broad to be a market thesis by itself. A founder building for customer service is in a different adoption curve from a founder building finance approvals, autonomous outbound sales, code refactoring, research automation, or web-data operations. Salesforce’s Agentic Enterprise Index points to customer service, internal/business automation, and sales. LangChain points to customer service, research/data analysis, and internal workflow automation. McKinsey points to IT and knowledge management. The overlap is not random: these are workflows where inputs, tools, decisions, and handoffs can be bounded.

The third implication is that governance is becoming a product feature. KPMG says 65% of leaders cite agentic system complexity as the top barrier, 80% cite cybersecurity as the greatest barrier to AI strategy goals, 60% restrict agent access to sensitive data without human oversight, and 75% prioritize security, compliance, and auditability for agent deployment. Those numbers suggest a buying checklist: identity, permissions, tool catalogs, policy enforcement, observability, data lineage, human review, and rollback.

Which agent workflows survive the pilot?

The clearest early surface — LangChain’s most common primary use case at 26.5%, and a Salesforce top-three area. Queues, policies, account context, and escalation rules give the agent a bounded job.

Salesforce reports agents drafting emails, creating to-dos, sending meeting requests, querying and summarizing records, and creating cases — agents touching the operational layer, not just answering questions.

LangChain’s second use case at 24.4%. Sources, extraction targets, and reviewable outputs make this a strong web-data fit: collect public information, extract fields, compare pages, enrich a spreadsheet, monitor changes.

McKinsey’s most commonly reported agent surface, including service-desk management and research-style workflows. Tickets, runbooks, identity systems, and service-level expectations create a structured environment.

A major surface among technical teams — LangChain’s write-ins say coding agents dominate daily workflows, with Claude Code, Cursor, GitHub Copilot, Amazon Q, Windsurf, and Antigravity appearing often. Repos, tests, and review gates are the structure.

A domain-specific read on the first agent wave. Tap a workflow to see why it is a natural early candidate and where it still needs a human.

LangChain, Salesforce, McKinseyThe fourth implication is that production proof beats broad claims. If a vendor says “our agent automates sales,” a buyer will increasingly ask: Which records can it read? Which records can it write? Which actions require approval? How are failures detected? What does it do when source data conflicts? Can I see every tool call? OpenAI’s Agents SDK emphasizes orchestration, tool execution, approvals, and state. LangChain’s observability and evaluation data shows that production teams are building those muscles because they have to.

For operations teams, the practical playbook is to start with one repeatable workflow where the cost of a missed step is known and the value of speed is visible. Good candidates have structured outputs, clear source data, reviewable intermediate steps, and a natural human handoff. Web-data work is a good example: an agent can collect public information, extract fields, compare pages, enrich a spreadsheet, monitor changes, or prepare a CRM update, while a person approves the final action when the risk is high. The point is not to make the agent omnipotent. The point is to make the delegated slice reliable.

For founders, the same logic argues against vague horizontal positioning. A narrower agent with better data access, better permissions, and better evaluation can be more valuable than a broader agent that claims to do everything. Buyers in 2026 are learning the difference between a model that can reason through a task and a product that can run a workflow inside their company. The latter needs integrations, policy, memory, logging, admin controls, pricing that matches usage, and a clear path from pilot to scale.

The final implication is that practical agent opportunities may be less glamorous than the phrase “autonomous AI” suggests. For many businesses, the first valuable agents will not run the company. They will collect data, triage tickets, enrich accounts, summarize records, draft responses, route issues, monitor changes, prepare research, update structured fields, and ask for approval before high-risk actions. For operations teams, ecommerce teams, sales teams, and web-data teams, that is still a big deal. It turns agent adoption from a fuzzy future-of-work story into a queue of measurable workflows.

Reading Agent Adoption Data Honestly

When you compare AI agent statistics in 2026, read the metric before the percentage.

Survey adoption ≠ market share

79% / 62% / 51% come from different populations

PwC's 79% adoption, McKinsey's 62% experimentation-or-scaling, and PagerDuty's 51% deployed all come from surveys, but they ask different populations and use different maturity language.

PwC, McKinsey, PagerDutyProduction ≠ scale

52%–57.3% in production, 2% at scale

Google Cloud's 52% and LangChain's 57.3% suggest strong production momentum among AI-active or builder-heavy samples. Capgemini's 2% at-scale figure reminds us enterprise-wide maturity is much rarer.

Google Cloud, LangChain, CapgeminiEmbedding ≠ usage

40% of apps ≠ 40% delegate work

Gartner's 40% enterprise-app forecast tells us agents will appear inside software. It does not tell us how often users will delegate work to them, or whether outcomes will be measurable.

GartnerSpend ≠ transformation

$1.3T forecast, but not proof of work done

IDC's $1.3T 2029 forecast, Menlo's $37B 2025 enterprise gen-AI spend estimate, and Ramp's spend-based index explain market momentum. They do not prove an agent is safely completing work in a particular process.

IDC, Menlo, RampGeneral AI use is not agent adoption, but it is not irrelevant. Gallup, Asana, Microsoft, and Stanford HAI show that employees, leaders, and consumers are becoming more comfortable with AI. That comfort lowers the training barrier for agents. It does not remove the need for integration, permissioning, and measurement.

A simple test helps: ask what the statistic would let you safely claim in a sales deck. If the source says employees use AI at work, you can claim workforce readiness, not agent deployment. If the source says executives plan to increase budgets because of agentic AI, you can claim budget appetite, not realized ROI. If the source says agents are in production among AI-active organizations, you can claim production momentum in an already-engaged sample, not universal penetration. If the source gives a staged maturity breakdown, you can discuss the gap between pilots and scale.

The Bottom Line

AI agent adoption in 2026 is best described as early production with uneven scale. The high-end numbers are real enough to matter: 62% at least experimenting in McKinsey, 52% deploying in production in Google Cloud’s gen-AI-active sample, 57.3% in production in LangChain’s builder survey, 79% adopted in PwC’s executive survey, and 51% deployed in PagerDuty’s executive survey. But the caveats are just as real: 2% at scale in Capgemini, over 40% cancellation risk in Gartner, and clear governance issues from OWASP, NIST, KPMG, and LangChain.

The useful reading is not that agents are either hype or inevitable. It is that agents are becoming an enterprise software layer before most organizations have fully redesigned work around them. The winners will not be the teams with the boldest autonomy claims. They will be the teams that choose bounded workflows, connect the right data, narrow the permissions, trace the actions, evaluate the outputs, and make human handoffs obvious.

That is a more practical story than the usual autonomy debate. AI agents are already entering customer service, sales, research, coding, IT, and operations, but durable adoption depends on the unglamorous layer underneath: data quality, workflow design, controls, and measurement. For 2026 planning, the right question is no longer whether companies will try agents. They are already trying them. The better question is which agent workflows can be trusted enough to keep running after the pilot budget, the launch announcement, and the first wave of curiosity are gone.

Frequently Asked Questions

What percentage of companies are using AI agents in 2026?

It depends on the maturity word. McKinsey reports 62% of respondents are at least experimenting with AI agents, PwC says 79% report agents are already being adopted, and PagerDuty says 51% have already deployed agents. These come from different surveys and populations, so they measure interest and self-reported adoption rather than a single market-share number.

How many organizations have AI agents in production?

Google Cloud says 52% of executives at organizations already using gen AI report production AI-agent deployment, and LangChain’s builder-heavy survey finds 57.3% with agents in production. Both are production benchmarks within AI-active or technology-oriented samples, not universal penetration across all companies.

What share of companies have scaled AI agents across the enterprise?

Very few. Capgemini finds only 2% of organizations have deployed AI agents at scale, with 12% at partial scale, 23% having launched pilots, and 61% still exploring deployment. McKinsey adds that no individual business function has more than 10% of respondents reporting scaled agent use.

Where are AI agents being used first?

In bounded, information-heavy workflows. LangChain says customer service is the most common primary use case at 26.5%, followed by research and data analysis at 24.4% and internal workflow automation at 18%. Salesforce points to customer service, internal/business automation, and sales, while McKinsey highlights IT and knowledge management.

Why do AI agent adoption numbers differ so much between reports?

Because they measure different layers and populations. A broad executive survey captures interest, pilots, or adoption language; a builder survey like LangChain’s captures real production systems among teams close to the tooling (63% in technology, 49% at organizations under 100 people). Reading the metric and the sample before the percentage resolves most of the apparent contradiction.

How many AI agent projects are expected to fail?

Gartner predicts over 40% of agentic AI projects will be canceled by the end of 2027, citing escalating costs, unclear business value, and inadequate risk controls. Gartner also warns that many vendors are "agent washing" older automation or chatbots without substantial agentic capability.

How much will agentic AI spending reach?

IDC forecasts that AI spending driven by agentic AI-enabled applications and agentic-fleet management will reach $1.3 trillion in 2029, growing at 31.9% year over year from 2025. This measures market momentum and budget appetite, not proof that agents are completing work reliably in any given process.

Is general AI use at work the same as AI agent adoption?

No. Gallup finds 50% of U.S. employees use AI at work at least a few times a year, and Stanford HAI says generative AI reached 53% population adoption within three years, but those are broad AI-use figures. Agent adoption specifically requires a system with a goal, tool access, planning, and boundaries acting inside real workflows.

Sources and Further Reading

Enterprise adoption & deployment surveys

Forecasts, spend & market context

Definitions, governance & workforce