AI Startup Funding Statistics

Last updated on July 6, 2026

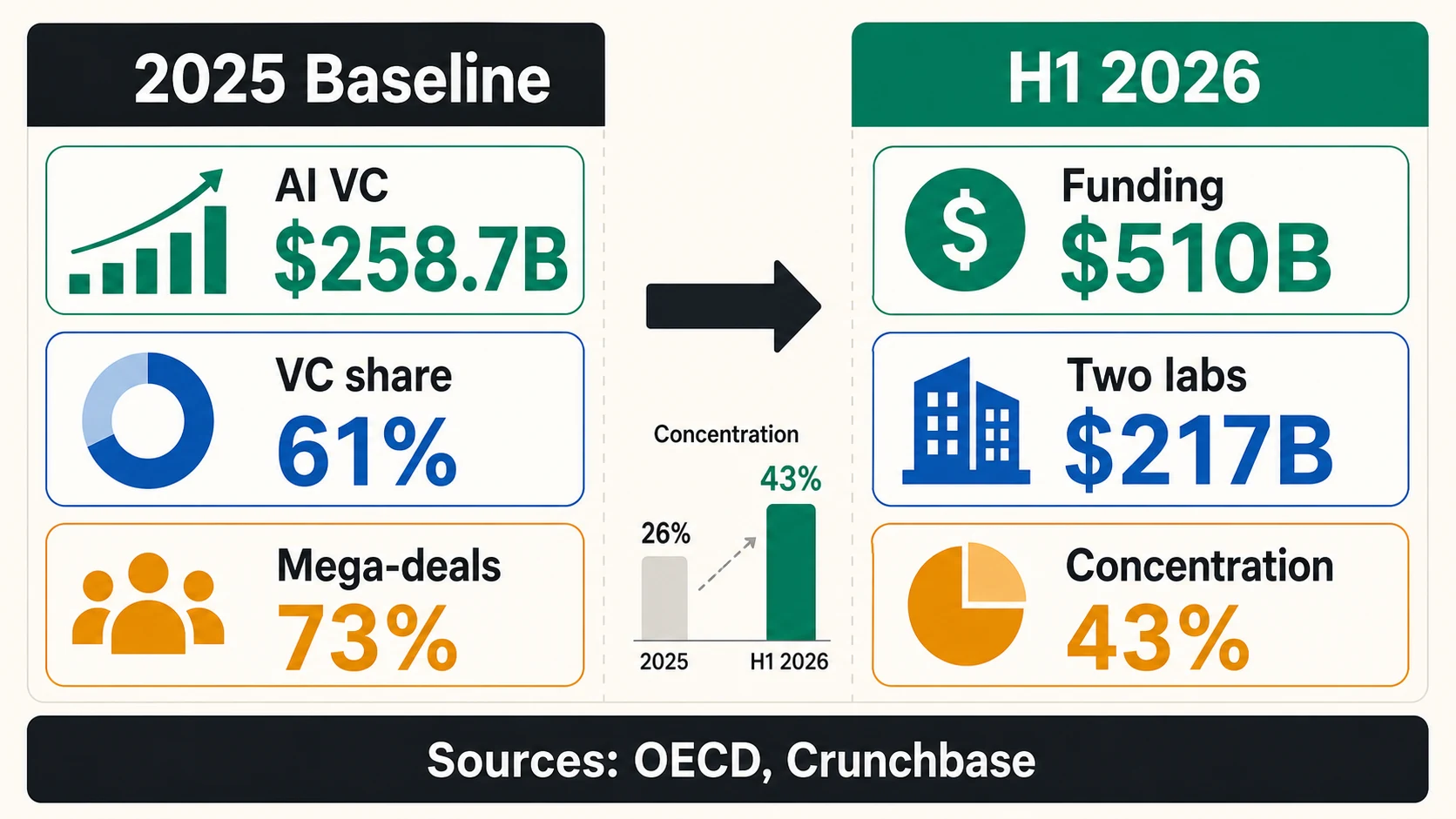

AI startup funding is no longer a side story in venture capital — it is the organizing principle of the market. In 2025, AI firms captured 61% of global venture capital investment, or $258.7 billion out of $427.1 billion, according to the OECD. Then the market accelerated again: Crunchbase reported $510 billion in global startup funding in the first half of 2026, with OpenAI and Anthropic alone accounting for $217 billion, or 43% of the total.

Those are huge numbers, and they are easy to misuse. “AI startup funding” can mean global VC into AI firms, broader private AI investment, U.S. venture deal value, a cap-table platform’s observed rounds, a strategic minority investment, or enterprise AI spending — each with a different denominator. A founder raising a seed round should not treat OpenAI’s $122 billion in committed capital as a normal fundraising comp. But the same founder should read what those mega-rounds reveal: investors are concentrating capital where AI needs compute, data, distribution, and infrastructure at a scale venture markets rarely had to finance before.

Here is the clearest way to read AI funding in 2026: VC share shows where capital is going, mega-rounds show concentration, infrastructure spend shows capital intensity, stage-level valuations show the premium founders can actually price, and enterprise spend shows demand — not fundraising probability. This guide breaks each down with the caveats that matter for founders, operators, and anyone putting funding data in a pitch deck.

AI Startup Funding, By The Numbers

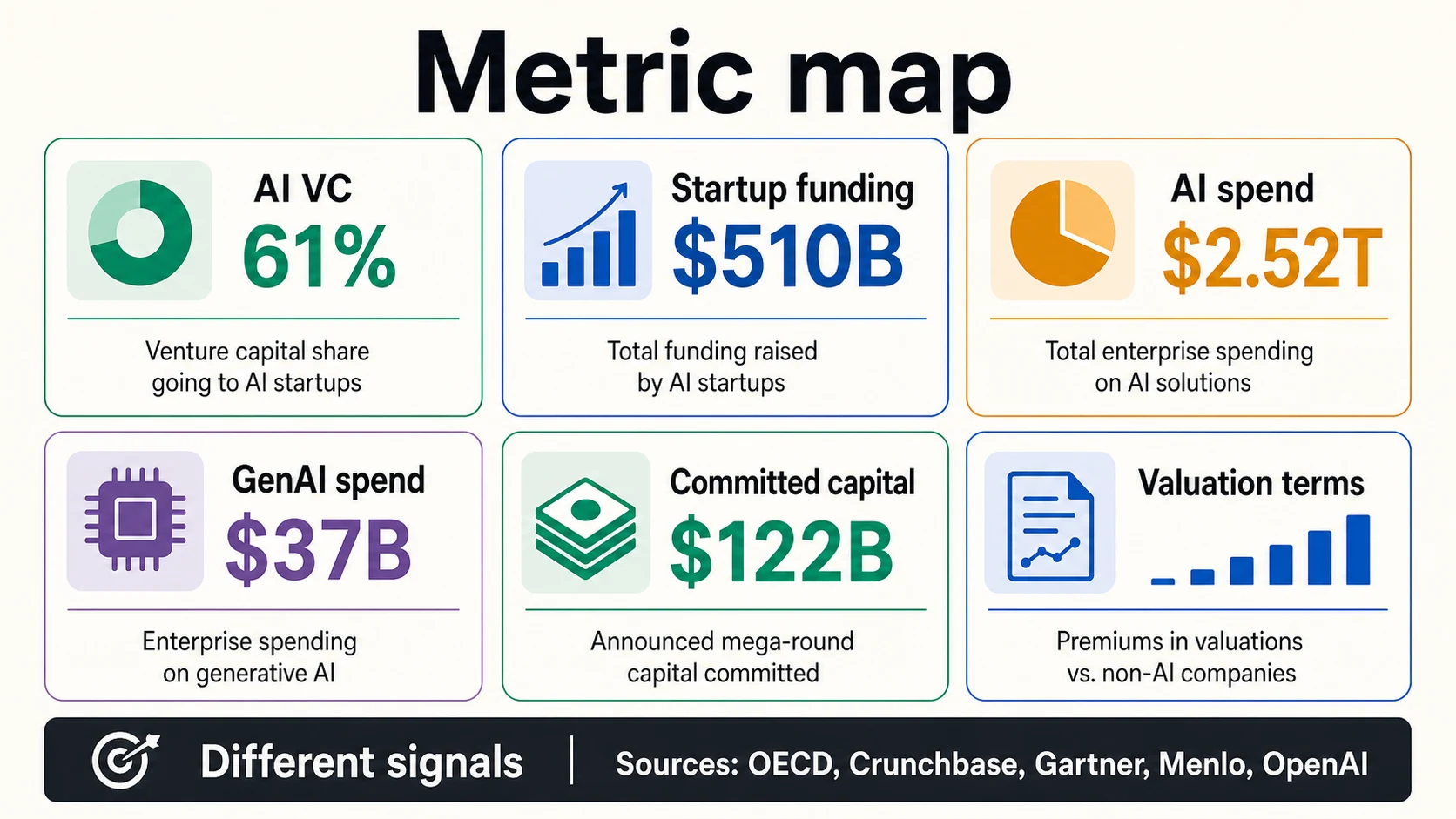

The headline AI funding figures use different denominators — global VC, all startup funding, U.S. deal value, platform samples — so read them as separate signals rather than one market-size total.

The market frame (VC & startup funding)

The demand frame (private investment & enterprise spend)

Read every number by its own denominator

Each AI funding headline answers a different question. Tap a metric to see what it measures — and what it does not prove.

OECD, Crunchbase, Stanford, GartnerAI Funding Is Huge, But The Definition Changes The Number

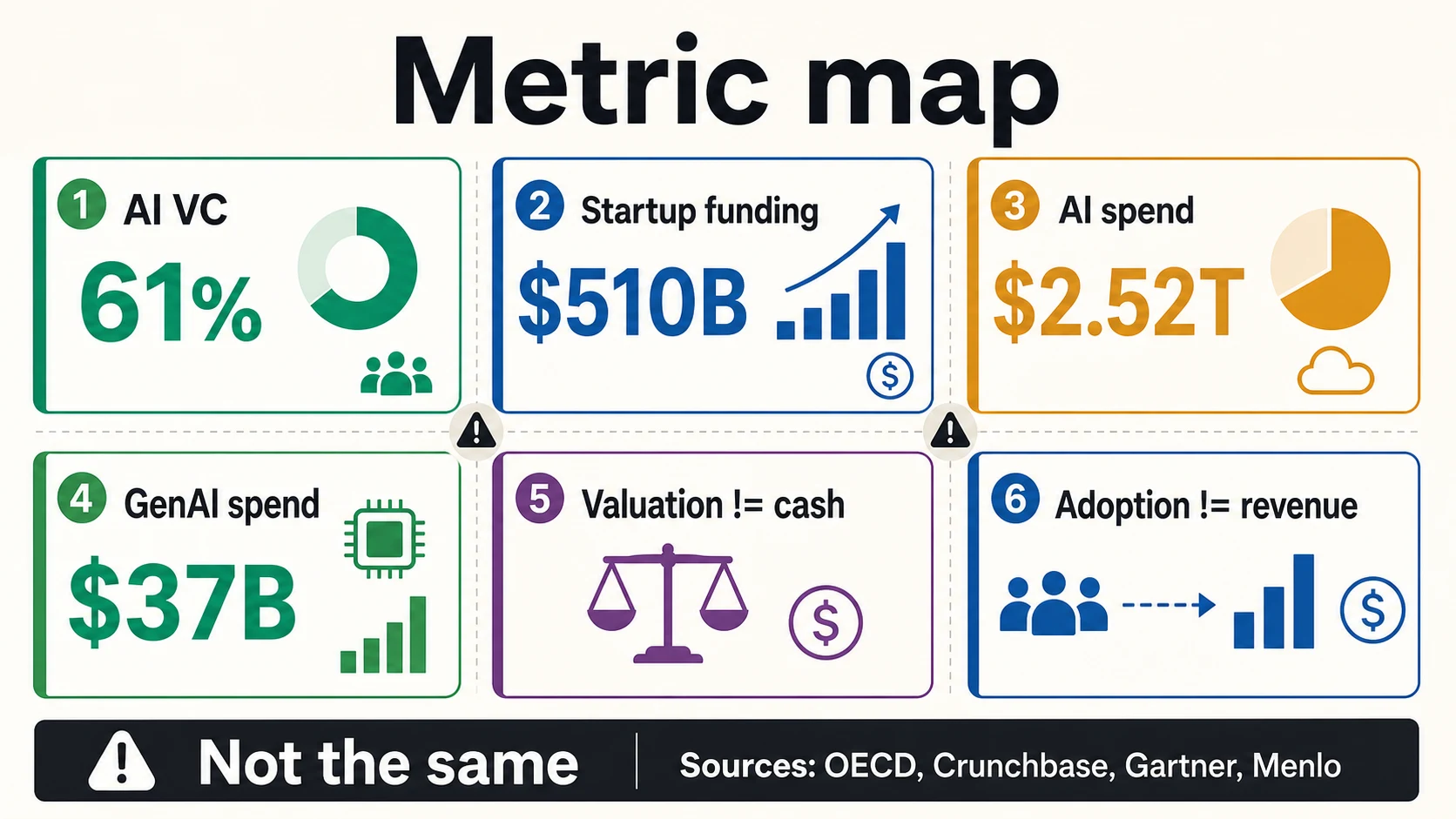

The cleanest place to start is the OECD’s 2025 venture-capital number: $258.7 billion invested into AI firms, representing 61% of global VC investment. That is a direct AI VC statistic. It does not include every form of private AI investment, every corporate infrastructure commitment, or every dollar enterprises plan to spend on AI systems.

Stanford’s 2026 AI Index uses a broader lens. It reports private AI investment and corporate AI investment, not only VC. That is why Stanford can report U.S. private AI investment of $285.9 billion in 2025 while the OECD reports $258.7 billion in global AI VC. Both can be true, because they are measuring different pools of capital.

Crunchbase is different again. Its H1 2026 article reports global startup funding across all categories, then highlights how much the total is being shaped by frontier AI companies. PitchBook/NVCA’s $267.2 billion Q1 2026 number is U.S. VC deal value, not global AI funding. Carta’s $30.4 billion Q1 2026 number is funding recorded among companies on Carta, not the entire market.

For founders, the practical rule is simple: cite the source and the metric together. “AI VC was 61% of global VC in OECD’s 2025 dataset” is a strong claim. “AI got most of all investment” is too vague. “Enterprise AI spending will be $2.52 trillion in 2026” is Gartner’s spending forecast, not a startup funding total.

AI VC

Global VC into AI firms

The tightest definition — 61% of global VC in 2025, or $258.7B. Best for a "why now" slide because it directly measures venture capital going to AI.

OECDPrivate investment

Broader than VC

Stanford's $285.9B U.S. figure counts private and corporate AI investment, a wider pool than OECD's VC-only view — so the two totals differ by design.

Stanford AI IndexStartup funding

All categories, then AI-shaped

Crunchbase's $510B H1 2026 total spans every startup category; frontier AI companies just dominate the mix.

CrunchbaseAI spending

Demand, not funding

Gartner's $2.52T is total AI spending across infrastructure, services, software, and providers — a buyer-budget number, not a fundraising total.

GartnerThe 2025 Baseline: AI Took A Majority Share Of VC

The 2025 VC baseline is striking because it shows AI moving from a hot category to the organizing principle of venture capital. The OECD reports that AI’s share of global VC doubled from 30% in 2022 to 61% in 2025. The same report says total VC investment in AI firms rose from $123.6 billion in 2023 back to $258.7 billion in 2025, roughly recovering to the 2021 peak in nominal terms.

Total VC into AI firms — 2023 to 2025

OECD's two reported anchors on a linear axis: global VC into AI firms more than doubled in two years, from $123.6B in 2023 to $258.7B in 2025 — 61% of all VC. This is the dollar series behind the share-of-VC story below.

OECDAI share of global venture capital

AI firms' share of all VC investment, on OECD's taxonomy. Source: OECD venture capital investments in AI through 2025.

Generative AI is important, but it is not the whole AI market. The OECD says VC investment in generative AI firms rose from $2.8 billion in 2022 to $15.3 billion in 2023, then to $35.3 billion in 2025, equal to about 14% of total AI VC. That means most AI VC, by OECD’s taxonomy, still sits outside the narrow GenAI bucket.

Stanford’s broader private-investment view shows the same upward pressure from another angle. The 2026 AI Index says private investment grew 127.5% and now accounts for 60% of global corporate AI investment. It also says generative AI captured nearly half of private AI funding and that newly funded AI companies rose 71%.

CB Insights’ 2025 AI report adds a company-concentration lens. It says OpenAI, Anthropic, and xAI raised $86.3 billion in 2025, equal to 38% of total AI funding in its dataset. That is not a small-company fundraising story. It is a story about a funding market where a few frontier labs can reshape the aggregate chart.

The 2026 Signal: A Record Market, Dominated By A Few Rounds

The clearest current signal is Crunchbase’s H1 2026 update, published July 2, 2026. Crunchbase reports $510 billion in global startup funding in the first half of 2026, surpassing the $440 billion it recorded for all of 2025. That is a major recovery at the top of the market.

But Crunchbase also says OpenAI and Anthropic accounted for $217 billion, or 43%, of all startup funding in H1 2026. In Q1 alone, Crunchbase says OpenAI, Anthropic, xAI, and Waymo collectively raised $188 billion, or 65% of global venture investment in the quarter.

That is the statistic founders should sit with. The market can be at a record high and still be narrower than the headline suggests. If two companies account for 43% of H1 funding, the average seed founder should not infer that capital has become easy. The better inference is that investors are willing to write extraordinary checks when the company sits at the center of frontier models, compute, distribution, or strategic infrastructure.

PitchBook/NVCA’s Q1 2026 Venture Monitor makes the same point from the U.S. market. The headline number, $267.2 billion in U.S. VC deal value, is enormous. But the NVCA summary says that excluding the five largest deals reduces deal value by 73.2%. PitchBook’s own webinar framing warns that AI-driven concentration can obscure broader uncertainty.

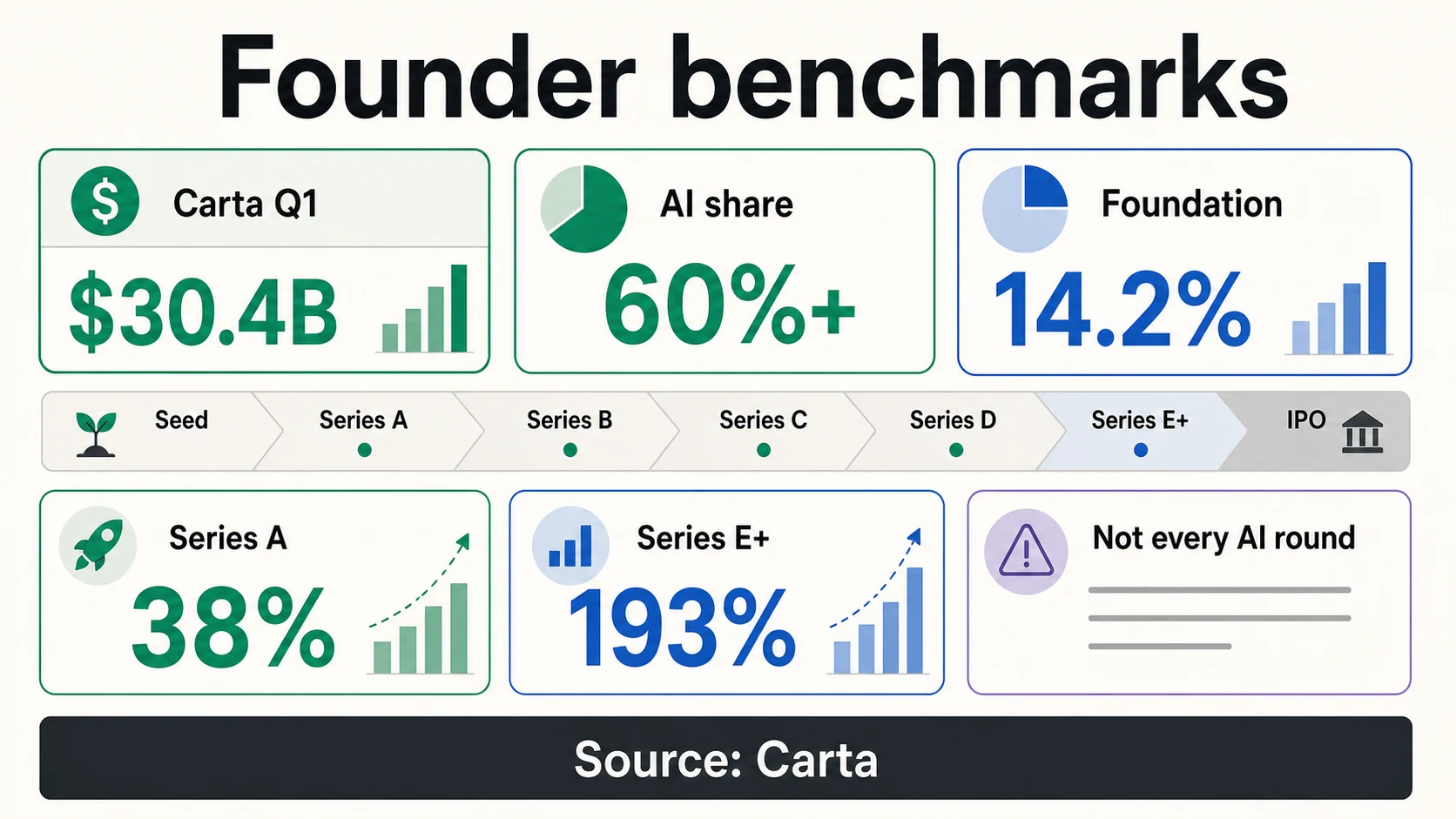

Carta’s Q1 2026 data shows what that looks like inside a startup platform sample. More than 60% of funding on Carta went to AI companies, and foundation-model companies alone drove 14.2% of total capital and nearly a quarter of AI capital. Carta’s warning is direct: a foundation-model Series A at a $300 million median valuation is not comparable to a non-AI Series A at $55 million.

Mega-Rounds Are Rewriting What “AI Startup Funding” Means

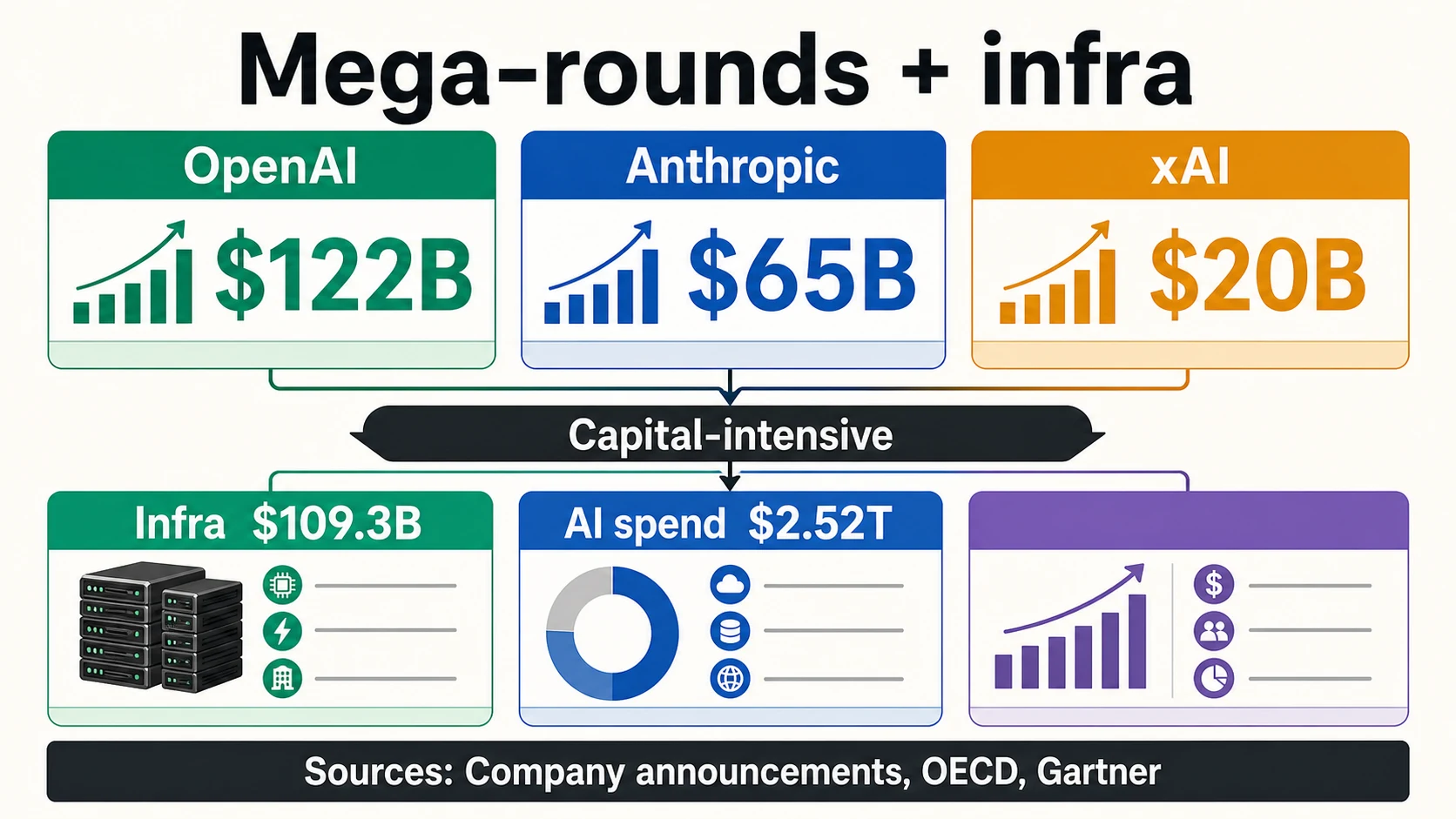

OpenAI’s March 2026 announcement is the biggest example of why wording matters. OpenAI said it closed $122 billion in committed capital at an $852 billion post-money valuation. “Committed capital” is not the same phrase as “immediate unrestricted cash,” and a founder should not rewrite it that way in a deck.

Frontier-lab mega-rounds (company announcements)

Anthropic announced a $65 billion Series H at a $965 billion post-money valuation in May 2026. It had already announced a $13 billion Series F at a $183 billion post-money valuation in September 2025. xAI announced a $20 billion Series E and named strategic investors including NVIDIA and Cisco Investments.

The pattern is not limited to U.S. labs. Mistral AI announced a €1.7 billion Series C at an €11.7 billion post-money valuation in September 2025. ASML said it invested €1.3 billion in that round and would hold about 11% of Mistral on a fully diluted basis. That is a strategic industrial AI investment as much as it is a startup funding headline.

Other large AI-company financings have different structures. Databricks announced a $10 billion expected non-dilutive financing in late 2024, with $8.6 billion completed and a $62 billion valuation. In 2025 it announced a Series K term sheet valuing the company above $100 billion and later said it was raising more than $4 billion at a $134 billion valuation while crossing a $4.8 billion revenue run-rate. These are strong signals, but “non-dilutive financing,” “valuation,” and “revenue run-rate” each mean something different.

Scale AI’s 2025 transaction with Meta is another useful caution. Scale announced a significant Meta investment that valued Scale at over $29 billion, expanded the commercial relationship, and provided liquidity to shareholders and vested equity holders. A liquidity-heavy strategic investment is not the same thing as a classic primary venture round for operating capital.

Infrastructure And Compute Are Pulling Capital Upstream

The AI funding boom is partly a software story, but increasingly it is an infrastructure story. The OECD reports that AI firms in IT infrastructure and hosting attracted $109.3 billion in VC investment in 2025, more than 42% of all AI VC in its category breakdown. That one number explains why many AI funding headlines feel different from the SaaS funding headlines of the 2010s.

Training and serving frontier models requires capital-intensive compute. xAI’s announcement explicitly connects its Series E to strategic investors and GPU-cluster buildout. CoreWeave’s public results show the demand side of the AI cloud boom: the company reported $5.131 billion in 2025 revenue and $66.8 billion in revenue backlog. Its S-1 describes a business built around large-scale AI infrastructure rather than ordinary software margins.

Gartner’s 2026 forecast reinforces the infrastructure pull. Gartner expects worldwide AI spending to reach $2.52 trillion in 2026, up 44% year over year, and says AI infrastructure will add $401 billion in spending as technology providers build AI foundations. That number is not startup funding. It does, however, explain why capital is flowing into cloud capacity, chips, data centers, data infrastructure, and model platforms.

For application-layer founders, this changes the pitch. It is no longer enough to say “AI is hot.” Investors will ask whether the business is capital-efficient or compute-heavy, whether margins improve with model costs, whether data access is defensible, and whether incumbents can bundle the same feature into existing workflows. The macro data helps, but the company-level answer matters more.

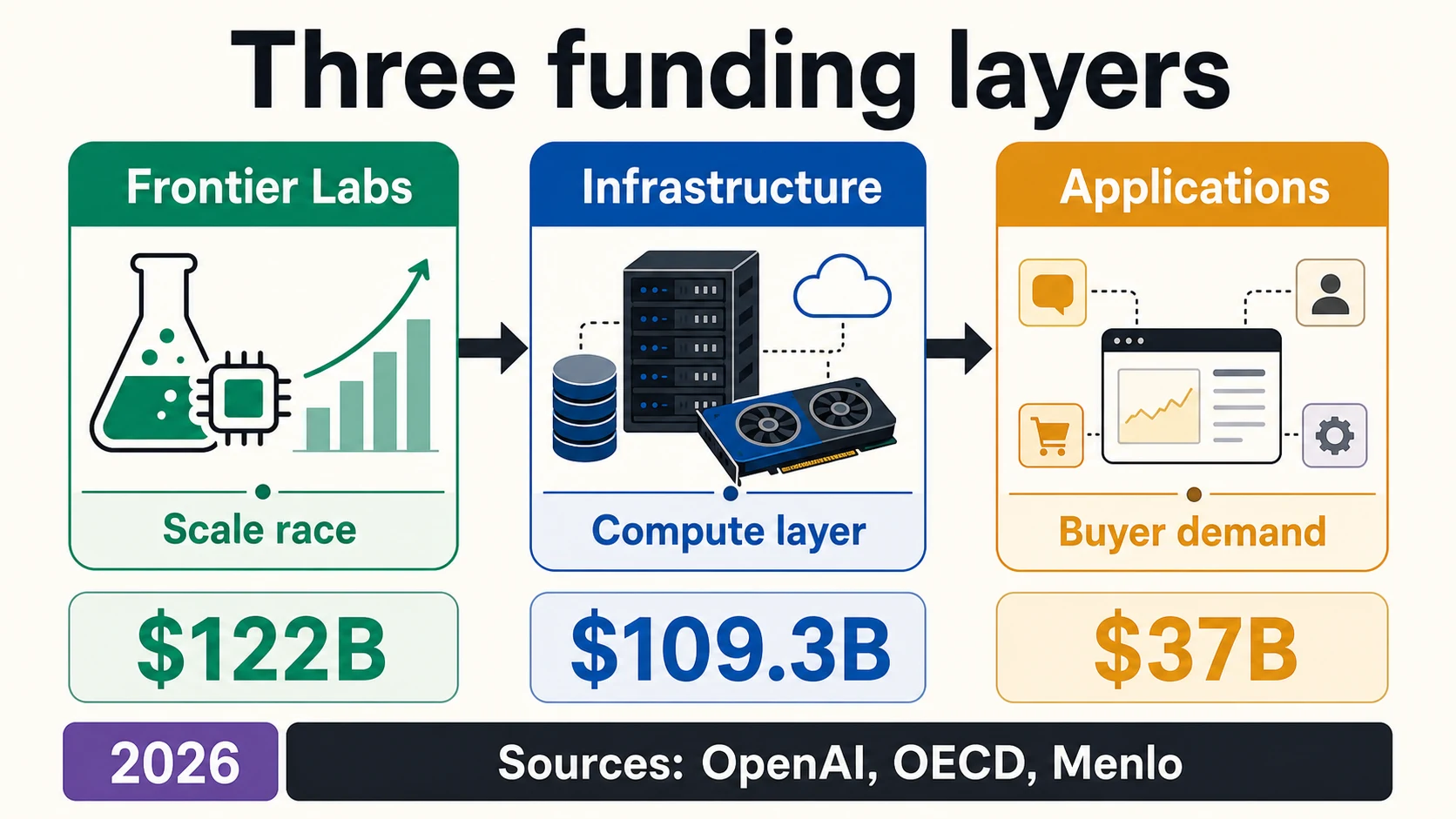

The Three Layers Of AI Startup Funding

The most useful way to read the 2026 funding market is not one line labeled “AI.” It is three layers: frontier model labs, AI infrastructure, and AI-native applications. Dealroom’s live AI guide uses a similar split, describing foundation model labs, AI infrastructure, and AI-native applications as structurally different markets with different round-size profiles and capital needs.

Three layers, three fundraising questions

Companies training or serving frontier models, where every generation needs more compute, data, and distribution. OpenAI’s $122B committed capital, Anthropic’s $65B Series H, and xAI’s $20B Series E are closer to private-market infrastructure races than normal startup rounds.

AI clouds, data centers, model serving, chips, data infrastructure, labeling, evaluation, security, and developer platforms. OECD’s $109.3B infrastructure/hosting figure and CoreWeave’s $66.8B backlog sit here. These companies may raise equity, but also debt, project finance, and strategic partnerships.

Companies using models to automate sales, support, coding, legal, healthcare, finance, ecommerce, research, and web data extraction. The largest layer by company count, but round sizes are usually smaller. Menlo says $19B of 2025 enterprise GenAI spend went to application-layer products and software.

AI funding is best read as a stack, not one line. Tap a layer to see its capital profile and the question investors actually ask.

Dealroom, OECD, OpenAI, MenloThe first layer is the frontier model lab. This includes companies training or serving frontier models, where every new generation can require more compute, more data, larger research teams, and more distribution. OpenAI’s $122 billion in committed capital, Anthropic’s $65 billion Series H, and xAI’s $20 billion Series E are not normal startup rounds. They are closer to private-market infrastructure races with venture, strategic, and corporate capital mixed together.

The second layer is AI infrastructure — AI clouds, data centers, model-serving infrastructure, chips, labeling, evaluation, security, observability, and developer platforms. OECD’s $109.3 billion infrastructure figure, CoreWeave’s $66.8 billion backlog, and Scale AI’s Meta-backed transaction all sit in this wider story. These companies may raise equity, but they may also use debt, project finance, strategic partnerships, or commercial commitments.

The third layer is AI-native applications — companies using models to automate sales, customer support, coding, legal review, healthcare workflows, finance operations, ecommerce, research, marketing, web data extraction, and internal enterprise work. This is where the number of startups is highest, but round sizes are usually smaller than the frontier-lab and infrastructure layers. Menlo’s enterprise GenAI report is helpful here because it says $19 billion of 2025 enterprise GenAI spend went to application-layer products and software.

Each layer has a different fundraising question. A frontier lab has to explain whether it can keep up with compute and distribution. An infrastructure company has to explain utilization, backlog quality, capacity, financing structure, and customer concentration. An application company has to explain why the product is not just a thin wrapper, how the workflow changes, and why the buyer will keep paying after the novelty wears off.

How AI Funding Changes Round Strategy

The funding boom does not remove the old fundraising questions. It makes them sharper. Carta’s 2025 review says startups on its platform raised more capital in 2025 while round count fell to the lowest level in at least six years. That means capital was available, but it was not spread evenly. Investors were choosing fewer companies and writing larger checks into the ones they believed could compound.

For pre-seed founders, the macro numbers can be more distracting than helpful. Carta’s pre-seed data shows a market still shaped by SAFEs, convertible notes, valuation caps, and modest round bands: $10.4 billion across 50,316 SAFEs and convertible notes, with valuation caps around $10 million for smaller post-money SAFE rounds and $15 million for larger ones. That is a very different world from OpenAI’s committed-capital announcement.

Infrastructure-heavy: finance capacity before revenue.

The round may need to fund compute, data centers, or capacity ahead of full revenue — investors will probe utilization, backlog, and financing structure.

Application-layer: tie the round to repeatable GTM.

Show usage depth, paid conversion, workflow ownership, and strong unit economics — plus a reason the buyer will not wait for an incumbent to bundle the feature.

Data-heavy: prove the advantage is durable.

The investor question is whether your data access is legal, defensible, and hard to replicate — not just that you have data today.

Agentic automation: reliability is the raise.

Reliability, governance, error handling, and whether the agent works inside real business constraints. Deloitte says only one in five companies has mature governance for autonomous agents.

For seed and Series A founders, the question is whether AI changes the milestones required to raise. Investors now often expect faster product velocity because AI reduces the cost of prototyping — but also sharper evidence, because AI features are easy to copy. A founder raising an AI application round should be ready to show usage depth, paid conversion, workflow ownership, proprietary data access, measurable time savings, and a reason the buyer will not simply wait for Microsoft, Google, Salesforce, ServiceNow, Adobe, or a vertical incumbent to bundle the same feature.

For growth-stage companies, the AI premium can be real but unforgiving. Carta’s 193% Series E+ AI valuation premium shows investors are paying for late-stage AI winners. But that premium sits alongside PitchBook/NVCA’s warning that excluding the five largest Q1 2026 deals dramatically changes the market picture. The growth market is open for companies that look like category-defining AI platforms; it is not open equally for every company that added an AI feature. Deloitte’s finding that only one in five companies has mature governance for autonomous agents is a reminder that the buyer side is not frictionless.

Stage-Level Reality For Seed And Series A Founders

Aggregate funding totals are least useful when a founder tries to price a round. Carta’s 2025 data is more practical because it shows how AI premiums differ by stage. Carta says startups on its platform raised $119.5 billion in 2025, up 16.9% year over year, while total round count fell to a six-year low. That means more capital was flowing through fewer rounds.

Carta also reports that AI startups raised larger rounds and higher valuations than non-AI startups at every stage from Series A onward. At Series A, the AI median valuation premium was 38%; at Series E+, it reached 193%. That is a real premium, but it is not a license to copy late-stage frontier-model comps into an early application-layer raise.

The pre-seed market tells a quieter story. U.S.-based startups on Carta raised $10.4 billion across 50,316 SAFEs and convertible notes in 2025, with total cash down 1% and instrument count down 13% from 2024. Median valuation caps on post-money SAFEs hovered around $10 million for rounds between $250,000 and $1 million, and around $15 million for rounds between $1 million and $2.5 million.

That is the founder reality beneath the mega-round headlines. AI can help a company command a premium, but investors still care about stage, round size, ownership, dilution, milestones, burn, and whether the product earns its place in a buyer’s workflow. PitchBook/NVCA’s top-deal exclusion effect and Carta’s foundation-model caveat point in the same direction: the top of the AI market is not a normal benchmark for every startup.

Geography: The Boom Is U.S.-Led, Not Evenly Global

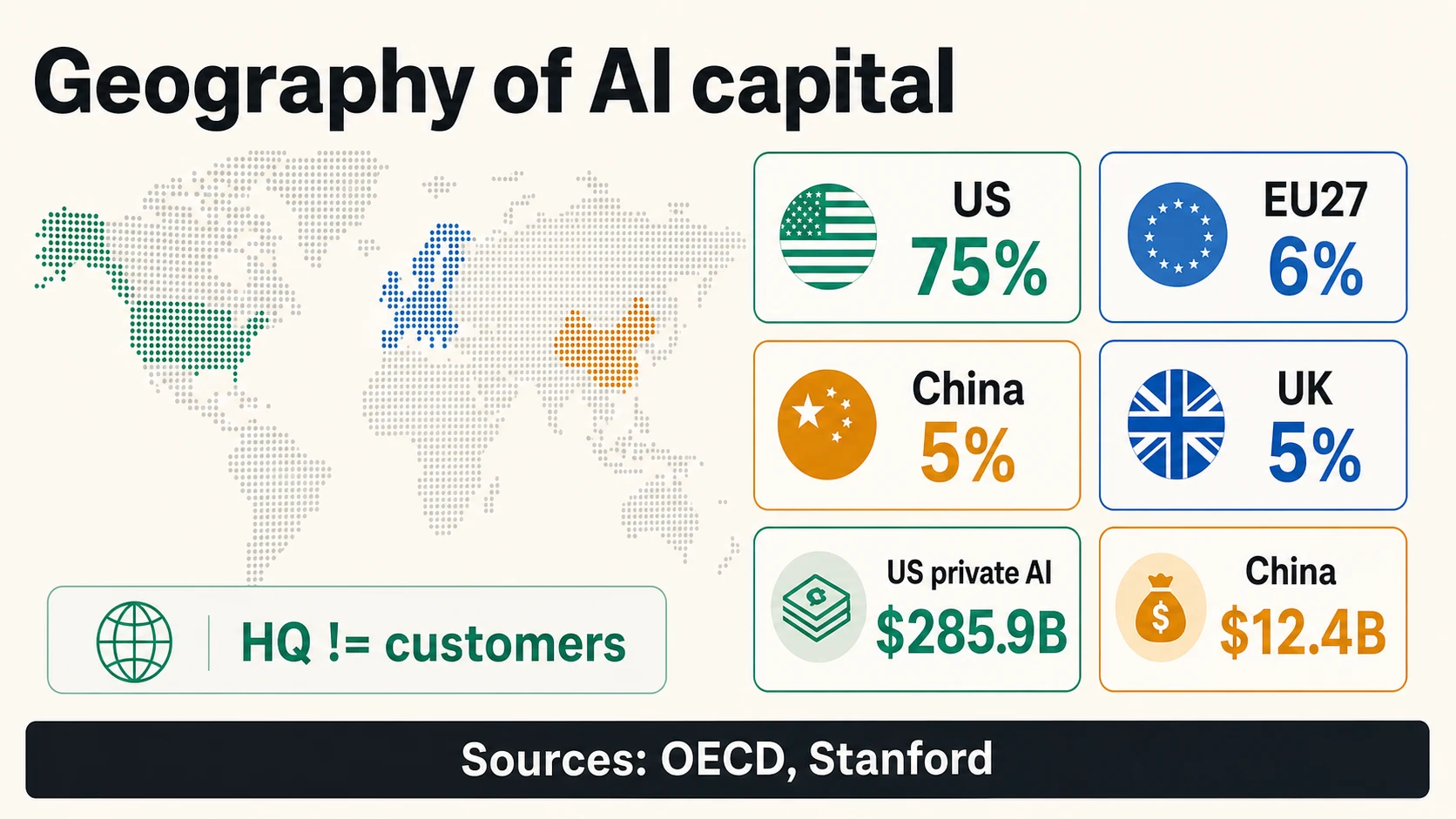

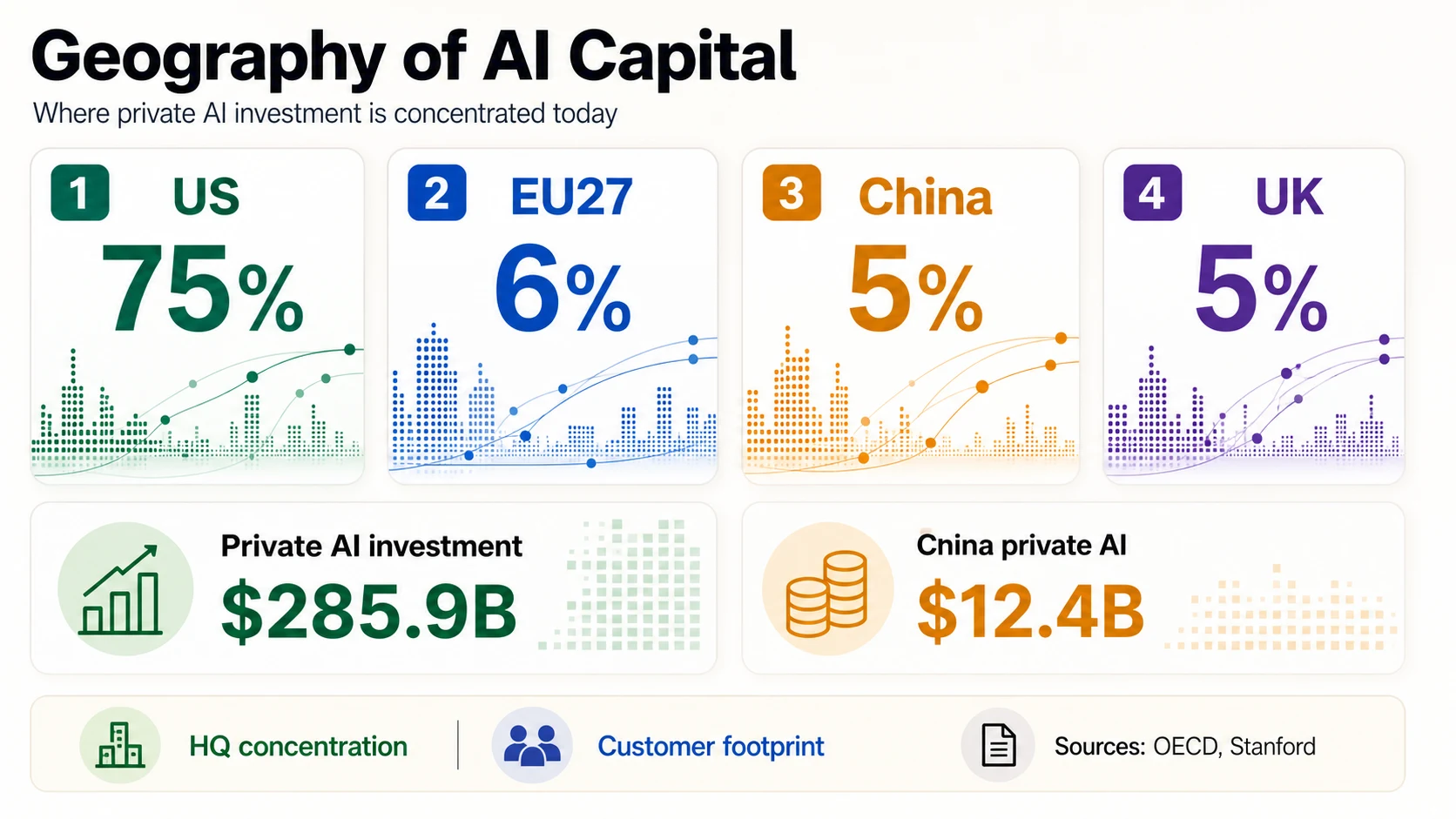

AI funding is global in attention, but not evenly distributed in capital. The OECD reports that U.S.-based AI firms attracted around $194 billion, or 75%, of global AI VC deal value in 2025. The next largest shares were much smaller: EU27 at 6%, China at 5%, and the U.K. at 5%.

Stanford reports a similar U.S. lead in private AI investment, with $285.9 billion in the U.S. versus $12.4 billion in China in 2025. But Stanford also warns that private investment figures can understate China because government guidance funds are not fully captured.

Crunchbase’s 2026 regional coverage likewise emphasizes that the current AI funding boom is heavily U.S.-headquartered. Dealroom’s live AI guide shows similar concentration in top U.S. hubs while also tracking London, Tokyo, Beijing, Paris, and other regions. Use these geography numbers carefully: headquarters funding is not the same as customer geography, revenue geography, or product opportunity.

For founders outside the U.S., the right takeaway is not “the market is closed.” It is that fundraising stories need to be more specific. A European AI founder can point to Mistral’s €1.7 billion round or ASML’s strategic investment, but should also explain why the company can win from its location: sovereign AI requirements, industrial customers, regulatory trust, local data, defense, healthcare, manufacturing, or distribution advantages.

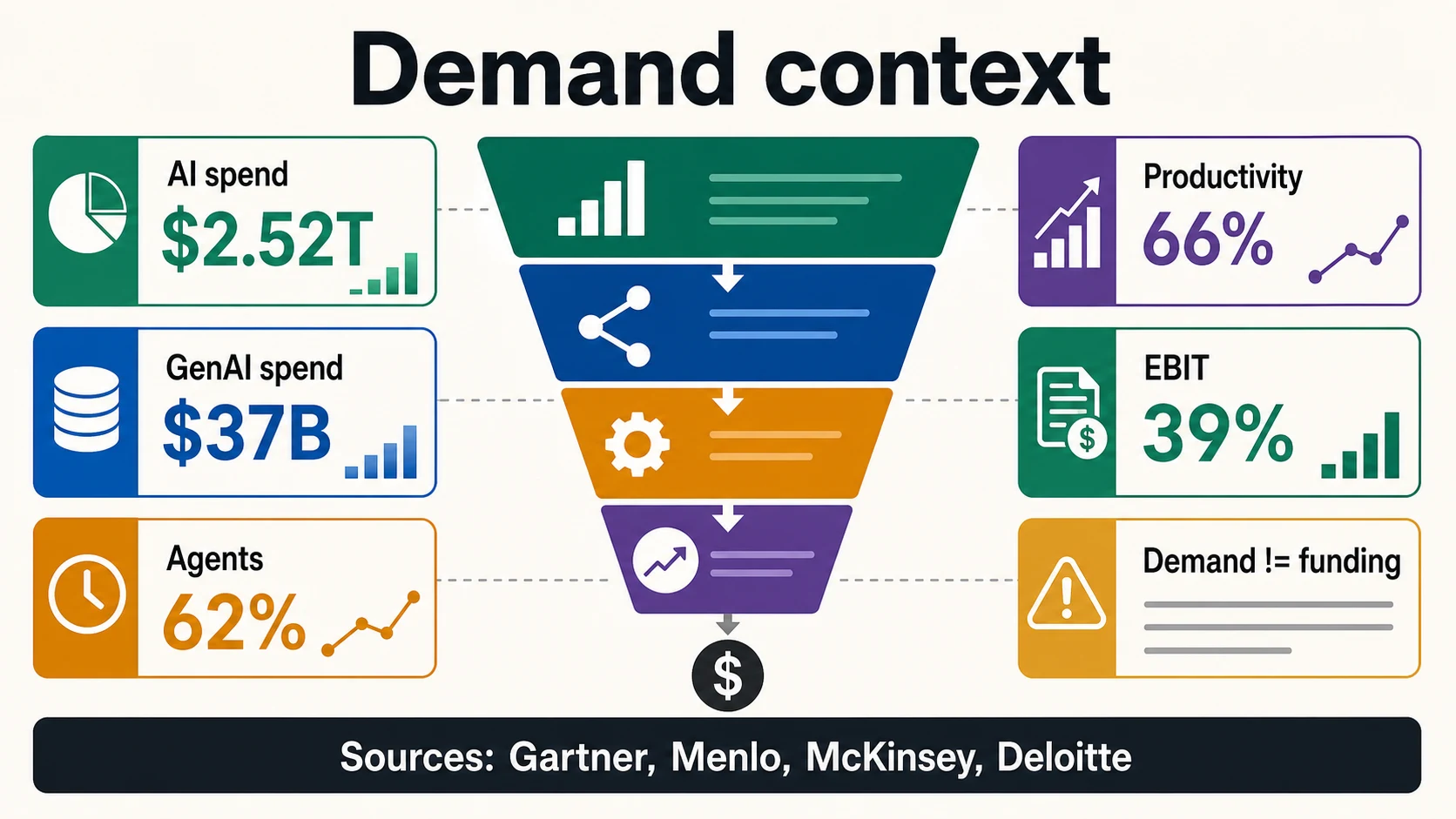

Enterprise Demand Explains The Funding, But It Is Not Funding

Investor appetite is easier to understand when enterprise demand is visible. Gartner forecasts $2.52 trillion in worldwide AI spending in 2026. Menlo Ventures estimates enterprise generative AI spend reached $37 billion in 2025, up from $11.5 billion in 2024, with $19 billion going to application-layer products and software.

McKinsey’s 2025 global AI survey says nearly nine out of ten respondents say their organizations are regularly using AI, 62% are at least experimenting with AI agents, and 39% report EBIT impact at the enterprise level. Deloitte’s 2026 State of AI report surveyed 3,235 leaders across 24 countries and reports that 66% of organizations have achieved productivity or efficiency gains, while only one in five has a mature governance model for autonomous AI agents.

These are useful demand signals. They are not proof that a startup will raise capital or capture revenue. Enterprise spend often flows to cloud providers, incumbents, consultants, cybersecurity, chips, infrastructure, internal teams, and software suites. A founder should use demand data to show why the category matters, then bring the conversation down to a specific buyer, workflow, budget, urgency, and measurable outcome. This is especially important for AI agents and automation companies: broad adoption says the market is paying attention, but it does not prove buyers will accept unreliable outputs, weak governance, unclear ROI, or tool sprawl.

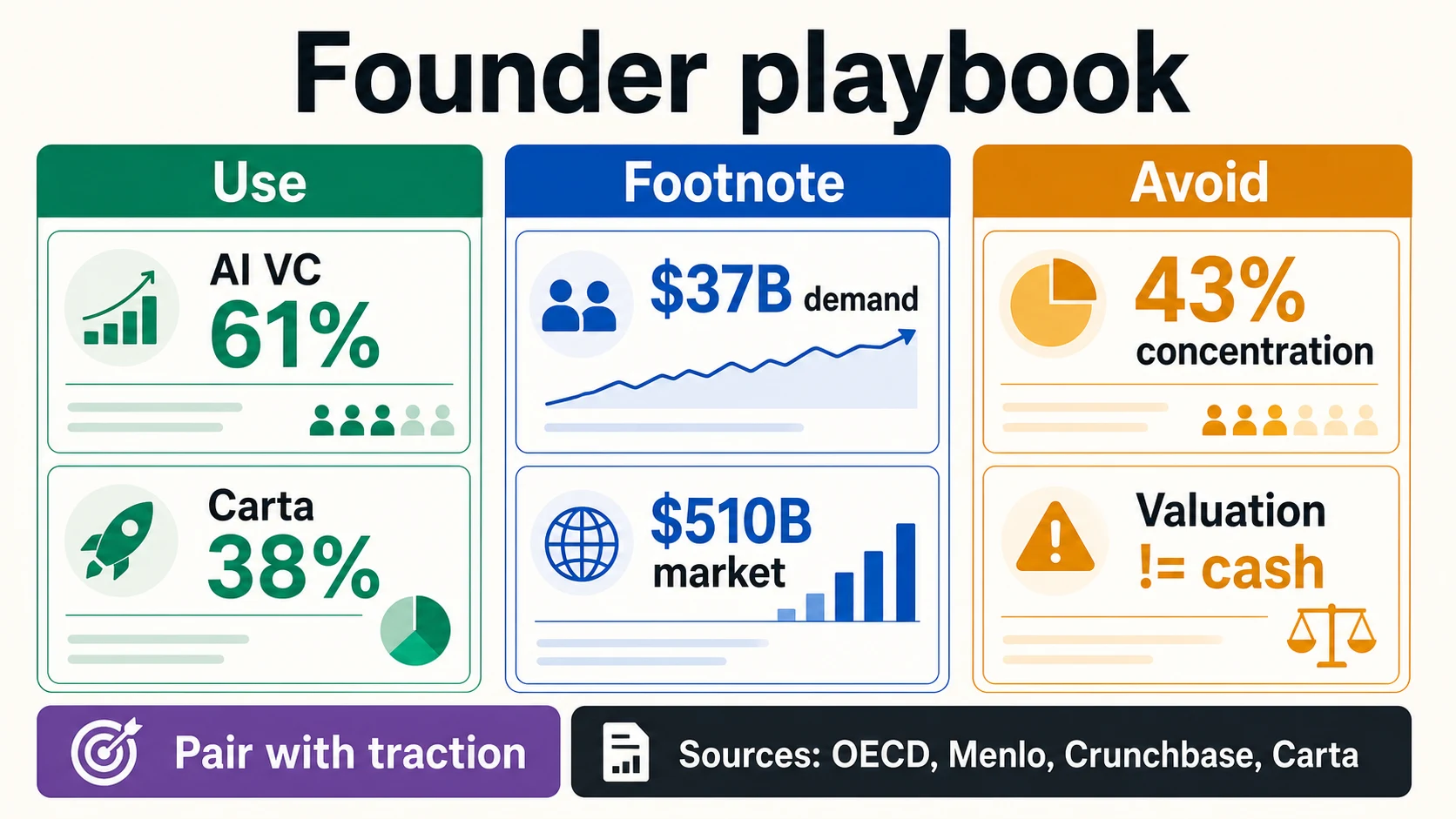

Pitch-Deck Statistics: What To Use, Footnote, Or Avoid

Not every impressive AI number belongs on the same slide. The strongest pitch-deck statistics are source-defined and directly relevant to the founder’s market. The weakest are dramatic totals borrowed from a different denominator.

Would this stat survive a due-diligence read?

A three-way sort for AI funding numbers headed into a pitch deck. Tap a bucket to see which statistics belong there and why.

OECD, Carta, Menlo, GartnerOECD’s 61% AI share of global VC is strong for a “why now” slide because it directly measures AI VC. Carta’s Series A AI premium is useful in fundraising conversations because it speaks to startup valuations in a platform dataset. Menlo’s $37 billion enterprise GenAI spend is useful when the product sells into enterprise AI budgets.

Some numbers belong in a footnote or a market-context slide. Gartner’s $2.52 trillion AI spending forecast is powerful, but it includes broad spending across infrastructure, services, software, and technology providers. It does not prove that an application startup can capture a specific budget. McKinsey’s adoption figures show widespread usage and experimentation, but also that many organizations are still early in scaling. Those are excellent setup facts, not closing arguments.

The best AI funding slide usually has fewer numbers, not more. One macro VC statistic, one demand statistic, one category-specific statistic, and one company-specific traction metric are usually stronger than a wall of giant market numbers. OECD proves AI is where VC is going; Menlo or Gartner shows buyer budgets are moving; Carta or PitchBook/NVCA shows the fundraising environment is concentrated; the startup’s own data shows why it deserves to be one of the companies funded inside that environment.

Reading Funding Numbers Without Overclaiming

Keep these distinctions attached to the numbers. Each pairs a common overclaim with the metric it actually is.

Denominator

AI VC ≠ private AI investment

OECD's $258.7B VC figure and Stanford's $285.9B U.S. private-investment figure measure different pools of capital, and generative AI funding is not the same as all AI funding.

OECD, StanfordScope

Global startup funding ≠ AI startup funding

Crunchbase's $510B H1 2026 total spans every category; the AI share is a subset, heavily concentrated in a few frontier labs.

CrunchbaseCash

Valuation and committed capital ≠ cash raised

A post-money valuation is not cash; committed capital is not always immediate unrestricted cash; secondary liquidity and cloud credits are not operating revenue.

OpenAISignal

Enterprise spend and survey adoption ≠ funding

Gartner's $2.52T spend and McKinsey's 88% adoption are demand and usage signals; platform samples like Carta are benchmarks, not global censuses.

Gartner, McKinseyFor 2026 specifically, also watch the date. The Crunchbase H1 update was published on July 2, 2026. Current-year private-market numbers can change as late-reported rounds enter databases. If you use a 2026 number in a deck or article, include the source and the date.

The Bottom Line

AI startup funding in 2026 is enormous, but the useful conclusion is not “all AI startups can raise easily.” The better conclusion is that capital has concentrated around frontier models, infrastructure, data, compute, and AI products with credible paths into enterprise workflows.

Frequently Asked Questions

How much did AI startups raise in 2025?

The OECD reports that AI firms captured $258.7 billion of global venture capital in 2025, equal to 61% of all VC investment, up from 30% in 2022. Stanford's broader private-investment measure puts U.S. private AI investment alone at $285.9 billion in 2025, because it counts a wider pool than VC.

What share of venture capital went to AI in 2025?

AI firms captured 61% of global venture capital in 2025, according to the OECD, up from 30% in 2022. That means AI moved from a hot category to a majority of all venture dollars in three years.

How concentrated is AI startup funding?

Crunchbase says OpenAI and Anthropic alone accounted for $217 billion, or 43%, of all global startup funding in H1 2026, and that in Q1 2026 OpenAI, Anthropic, xAI, and Waymo raised $188 billion, or 65% of global venture investment. The OECD adds that mega-deals over $100 million made up about 73% of 2025 AI investment value.

Which country leads AI startup funding?

The United States leads by a wide margin. The OECD reports U.S.-based AI firms attracted about $194 billion, or 75%, of 2025 global AI VC deal value, followed by the EU27 at 6%, China at 5%, and the U.K. at 5%. These shares are by company headquarters, not customer or revenue geography.

Why do AI funding numbers differ so much between sources?

Because they measure different things. OECD reports global VC into AI firms, Stanford reports broader private and corporate AI investment, Crunchbase reports all-category startup funding, PitchBook/NVCA reports U.S. VC deal value, and Carta reports funding among companies on its platform. Gartner's $2.52 trillion is AI spending, not startup funding at all.

How much bigger are AI startup valuations than non-AI startups?

In Carta's 2025 dataset, the median Series A valuation for AI startups was 38% higher than for non-AI startups, and at Series E+ the AI premium reached 193%. That is a real premium, but Carta warns it is a platform sample and that early rounds should not be priced off late-stage frontier-model comps.

Is enterprise AI spending the same as AI startup funding?

No. Gartner forecasts $2.52 trillion in worldwide AI spending in 2026 and Menlo estimates $37 billion in enterprise generative AI spend in 2025, but that is buyer demand, not venture funding. Enterprise AI spend often flows to cloud providers, incumbents, chips, and internal teams rather than startups.

What AI funding statistics should founders put in a pitch deck?

Use source-defined, directly relevant numbers: OECD's 61% AI VC share for "why now," Carta's Series A AI premium for valuations, and Menlo's $37 billion enterprise GenAI spend for demand. Footnote broad totals like Gartner's $2.52 trillion, and avoid presenting a valuation or committed-capital headline as cash raised.

Sources and Further Reading

Venture capital & startup funding data

Platform & stage-level benchmarks

Mega-round & infrastructure announcements

Private investment, spend & enterprise demand